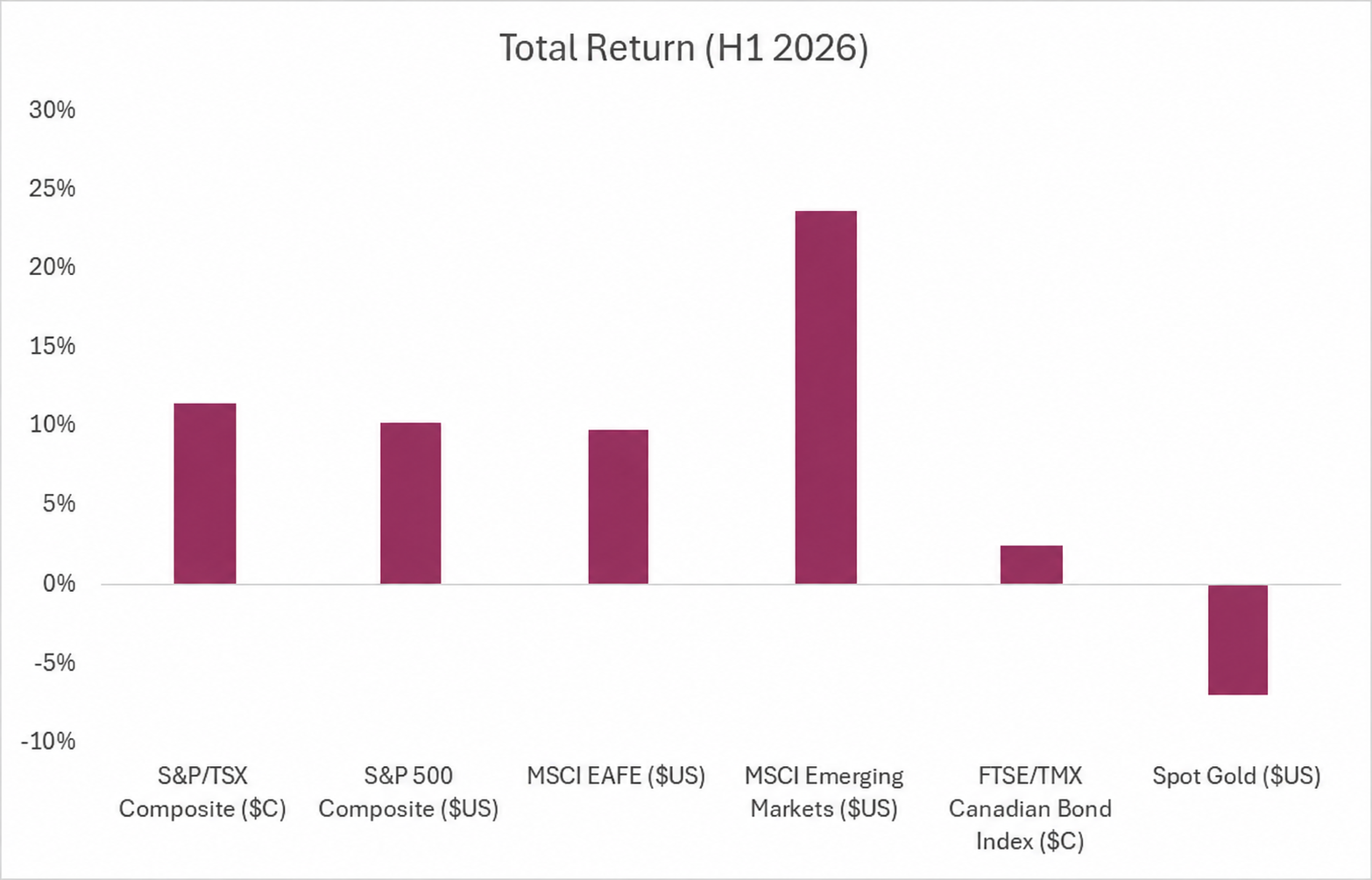

If the first half of 2026 proved anything, it was the remarkable resilience of financial markets. Despite geopolitical tensions, renewed inflation concerns and a brief selloff following the U.S.–Iran conflict, global equities recovered quickly. While headlines focused on geopolitics, investors remained focused on a much more important story: corporate earnings.

That focus has been justified. During first-quarter earnings season, 84% of S&P 500 companies exceeded analyst earnings expectations, well above the historical average. At the same time, analysts revised second-quarter earnings expectations higher throughout the quarter—an uncommon occurrence given estimates typically trend lower as reporting season approaches. Strong corporate profitability, led by continued AI investment and resilient business spending, has provided an important foundation for equity markets despite elevated valuations.

That shift has been particularly evident in emerging markets. Once viewed primarily as a play on commodities and energy, today's emerging market indices are increasingly driven by technology leaders in China, Taiwan and South Korea. As a result, the asset class has become closely tied to the AI investment cycle, providing a meaningful tailwind as investment in AI accelerates. The flip side, however, is that any moderation in AI spending or investor enthusiasm would likely be felt just as quickly.

While AI and corporate earnings dominated the equity narrative, inflation remained the market's biggest macroeconomic challenge. The U.S.–Iran conflict and concerns over potential disruptions to global energy supplies reinforced inflation risks, prompting investors to price in a more hawkish Federal Reserve. The resulting strength in the U.S. dollar created a headwind for gold, which gave back some of its early-year gains after surging out of the gates. However, the longer-term investment case remains intact, supported by persistent currency debasement, continued central bank buying and elevated geopolitical uncertainty.

The first half of the year was another reminder that the headlines dominating the news cycle — this time geopolitical flashpoints like the U.S.–Iran conflict — are rarely the same forces that drive market performance. Instead, corporate earnings, the continued AI investment cycle, monetary policy and evolving capital flows proved to be the more influential drivers and are likely to remain so in the second half of 2026.

Source: Bloomberg

Moving Forward

We've maintained a constructive view on equities in recent years, and despite periodic bouts of volatility, markets have continued to demonstrate remarkable resilience. But being constructive doesn't mean being complacent about risk. Every market cycle presents new challenges, and understanding where risks may emerge is critical to navigating them successfully. As we move into the second half of 2026, these are the key themes we're watching closely.

IPO Frenzy: Can Markets Absorb a Wave of New Supply?

One of the biggest market developments this year has been the resurgence of equity capital markets. During the first half of 2026, companies raised a record amount of capital through IPOs and secondary share offerings. SpaceX alone completed the largest IPO in history, raising approximately $75 billion, while established companies such as Alphabet also tapped public markets for additional capital.

The pipeline appears far from exhausted. Household names including OpenAI, Anthropic, ByteDance, Databricks, Stripe, Revolut and Canva are widely expected to pursue public listings over the coming quarters. Collectively, these companies could add an estimated $2–4 trillion in new public market capitalization, representing roughly 2.7% to 5.3% of the current $75 trillion Wilshire 5000 Index (which represents nearly the entire U.S. equity market). While not all of these companies are expected to list in 2026, the potential scale of the pipeline highlights a meaningful increase in the supply of publicly traded equities.

The question is whether markets can comfortably absorb this new supply. Unlike the past several years, when relatively few companies came to market, investors may soon face an abundance of new investment opportunities. Some capital will undoubtedly represent new inflows, while some may simply be reallocated from existing holdings.

The optimistic interpretation is that robust IPO activity reflects healthy investor demand and vibrant capital markets. A more cautious view is that an influx of new equity supply could temporarily pressure valuations as investors rotate capital into new listings. While the outcome remains uncertain, the market's ability to absorb this wave of new equity supply may become one of the defining themes of the second half of 2026.

The Fed's Tough Task Ahead

Kevin Warsh takes over as Chair of the Federal Reserve at a particularly challenging time. Inflation remains well above the Fed's 2% target, while economic growth has begun to moderate. At the same time, geopolitical uncertainty and evolving trade policy continue to cloud the inflation outlook, leaving policymakers with little room for error.

Although President Trump has been vocal in his desire for lower interest rates, Warsh has built his reputation as a proponent of sound money and has made it clear that restoring price stability remains his top priority. In fact, he has stated that he will not tolerate inflation above the Fed's 2% target. Until inflation shows more convincing signs of moderating, the Federal Reserve may have limited flexibility to support the broader economy.

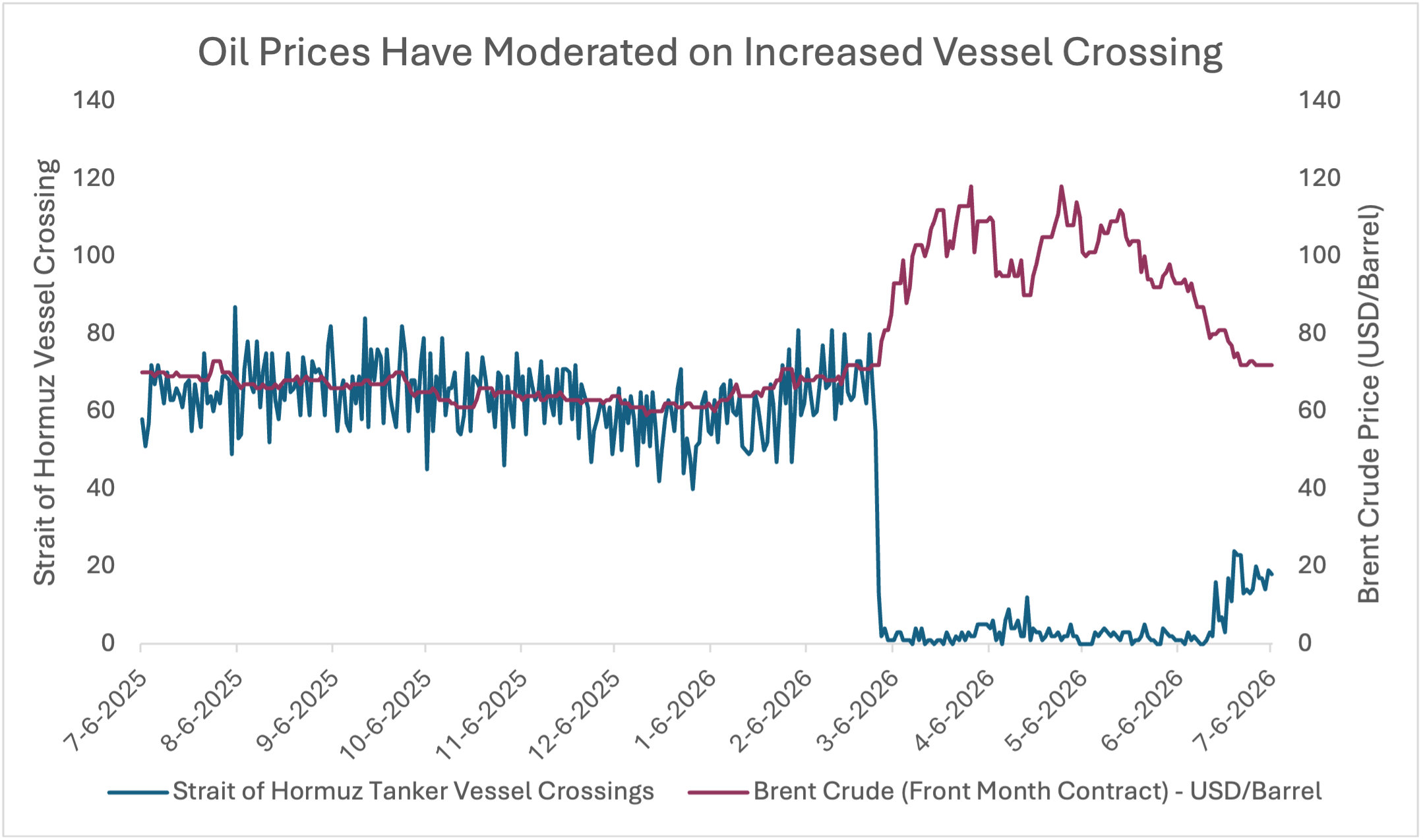

Energy prices remain a key variable. While shipping traffic through the Strait of Hormuz has partially normalized and oil prices have retreated from recent highs, the situation remains fragile — much of the calm rests on June's U.S.–Iran Memorandum of Understanding (MOU), the framework that reopened the strait and extended the ceasefire 60 days. A sustained ceasefire and uninterrupted energy flows would ease inflationary pressures and give the Fed greater room to lower rates. Conversely, with the ceasefire already tested by violations on both sides, any renewed breakdown could quickly reignite inflation concerns and delay a shift in monetary policy.

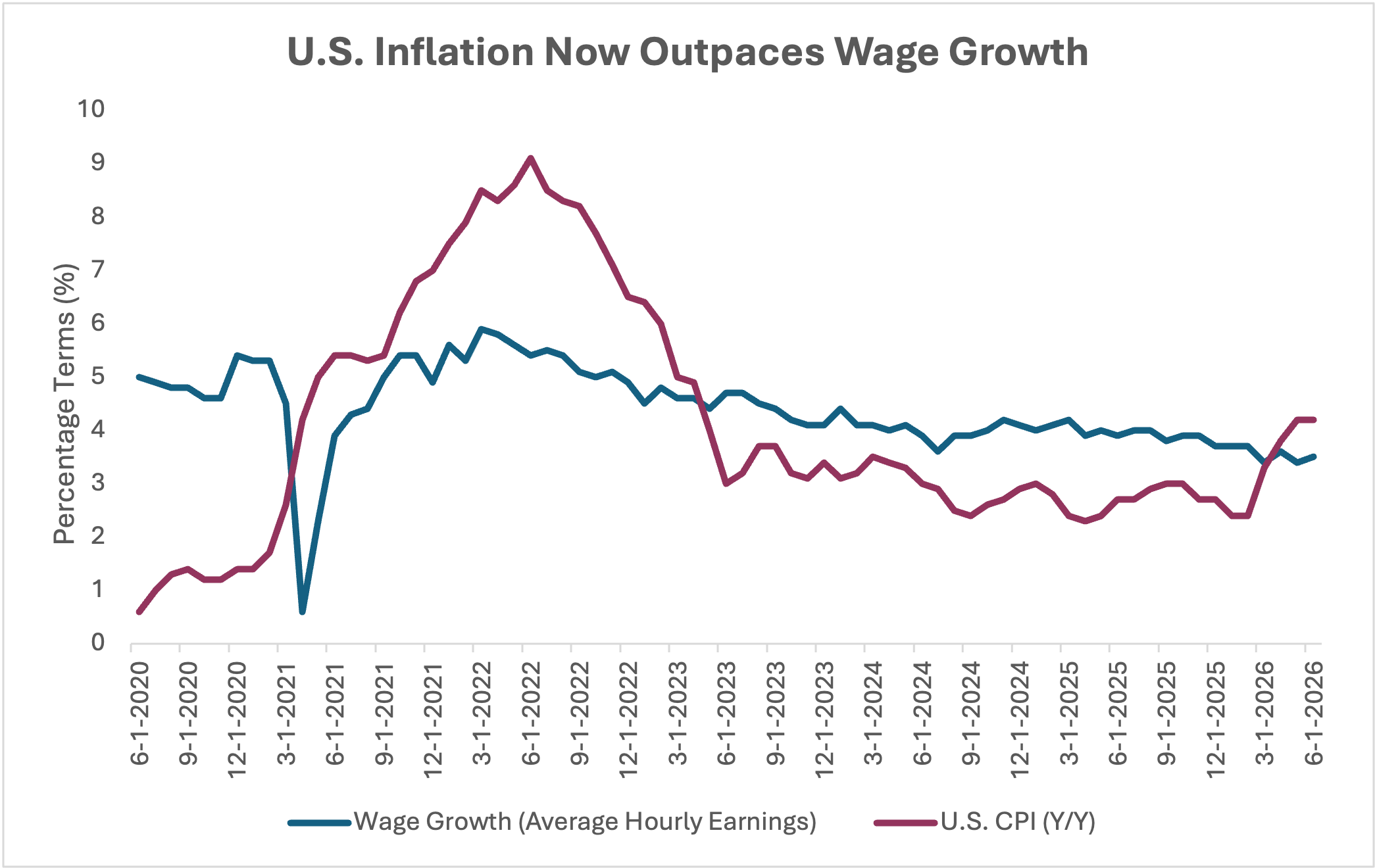

Adding to the challenge, inflation is once again outpacing wage growth. As shown in the below chart, U.S. CPI inflation (4.2%) has moved above average hourly earnings growth (3.5%), suggesting real purchasing power is beginning to erode. For investors, the direction of inflation—not just interest rates—may prove to be one of the most important drivers of markets during the second half of 2026, particularly as equity markets prepare to absorb a record pipeline of new public equity issuance.

Source: Bloomberg, Bureau of Labor Statistics (BLS)

Source: Bloomberg

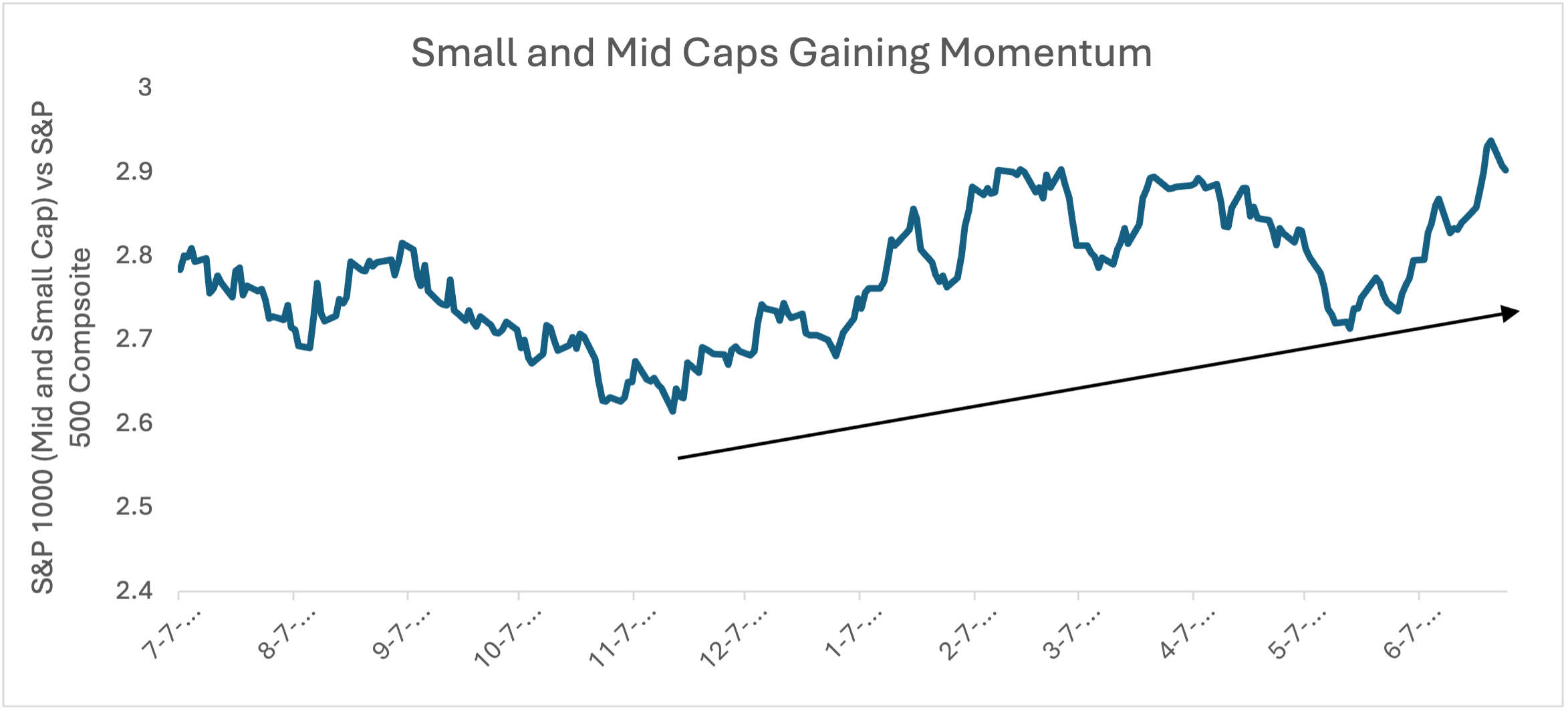

The Great Market Rotation

Earlier this year, we highlighted the extreme concentration within equity markets and suggested that conditions were becoming increasingly favourable for broader market participation. As discussed in our "Extreme Market Relationships: A Setup for Breadth" blog, periods of excessive concentration have historically been followed by a broadening of market leadership—and that's exactly what we've begun to see in 2026.

Two meaningful rotations have emerged this year. First, leadership has expanded beyond the Magnificent Seven, with a growing number of companies contributing to overall market performance. Second, investor interest has broadened beyond mega-cap stocks into mid- and small-cap companies, a constructive sign that confidence is spreading across the market rather than remaining concentrated in a handful of names.

From a technical perspective, improving market breadth is generally viewed as a positive development. Healthy bull markets are supported by broad participation across sectors and market capitalizations, making them less reliant on the performance of a few dominant companies. While AI continues to be a powerful structural driver, its benefits are increasingly extending beyond the largest technology companies to a wider range of industries.

Although leadership has broadened, we continue to view this as an evolution of the AI theme rather than a departure from it. As AI adoption expands, the opportunity set naturally broadens, allowing more companies—and ultimately more regions and sectors—to participate in the next phase of the market cycle.

Source: Bloomberg

Source: Bloomberg

Looking Forward: The Second Half of 2026

The first half of 2026 demonstrated the remarkable resilience of financial markets. Despite geopolitical uncertainty, evolving trade policy and persistent inflationary pressures, equities continued to advance while market leadership broadened beyond a narrow group of mega-cap technology companies.

Looking ahead, the second half of the year presents a new set of questions. Can markets absorb a record pipeline of IPOs and secondary offerings? Will inflation moderate sufficiently to give the Federal Reserve greater flexibility? And will the broadening of market participation continue as AI investment enters its next phase?

While these questions remain unanswered, they also reflect a market that is evolving rather than deteriorating. New capital formation, expanding market breadth and continued investment in transformative technologies are characteristics typically associated with healthy capital markets. At the same time, elevated valuations, geopolitical developments and monetary policy uncertainty remind us that volatility remains a normal part of investing.

As always, successful investing is not about predicting every short-term market move. It is about understanding the long-term forces shaping markets while remaining disciplined through periods of uncertainty. We will continue to monitor these evolving themes and provide timely insights as the investment landscape develops.