While the S&P 500 delivered its third consecutive year of 15%+ returns last year, looking beneath the surface reveals several notable extremes. Dissecting market leadership is always important in assessing the sustainability of a rally. Over time, leadership rotates — not only across sectors, but across factors and market capitalizations. When certain relationships become stretched to statistical extremes, they often serve as useful signals that the market may be setting up for a transition.

Today, three relationships stand out:

- High beta versus low volatility in U.S. equities is at an extreme, roughly a three-standard deviation move.

- Small Caps versus Large Caps (Russell 2000 / Russell 1000) remains near historic lows.

- The S&P 500 Composite relative to the Equal Weight S&P 500 Composite is also near historical highs, highlighting the concentration of market leadership.

Together, these extremes point to a highly concentrated market rally, where a narrow group of stocks and higher-risk segments have driven overall returns, while broader participation across styles and market capitalizations has lagged.

S&P 500 High Beta/S&P Low Volatility Ratio Trading at a Three Standard Deviation High

Russell 2000 (Small Caps) vs Russell 1000 (Large Caps) at a Historic Low

Three strong years in a row — can it continue?

As outlined in our 2026 Playbook iQ: New Year Outlook Report, the S&P 500 has delivered three consecutive years of returns above 15% — only the third time this has occurred historically. The natural question now is whether the rally can extend.

It can — but for returns to remain strong, the market likely needs to look different than it did last year.

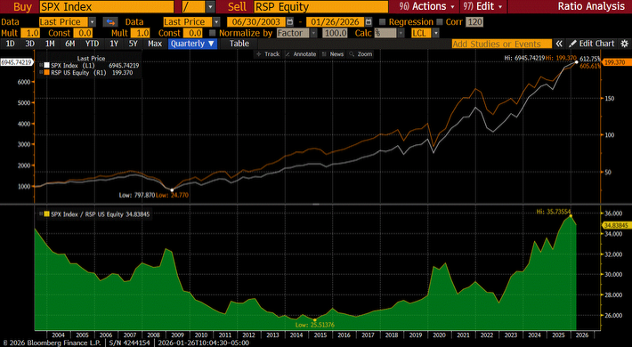

In 2025, leadership was highly concentrated, with a small group of Mega Cap AI-related stocks driving a disproportionate share of the index’s gains. One way to quantify this is through the relationship between Equal Weight and cap-weight indices: the ratio of the Equal Weight S&P 500 (RSP) relative to the traditional cap-weight S&P 500 remains near multi-decade lows. In other words, a narrow group of companies did most of the heavy lifting.

While a concentrated rally can persist longer than many expect, it also introduces fragility. When the market depends on a small number of names, it becomes more sensitive to shifts in positioning, sentiment, and volatility. If those leaders begin to lose momentum, there is limited participation elsewhere to sustain the advance.

S&P 500 Composite vs S&P 500 Equal Weight

The long-term backdrop remains constructive

We’ve argued for some time that the long-term environment continues to support a secular bull market in risk assets, largely driven by what we refer to as the ongoing debasement trade, which we will explore in more detail in a future blog.

Government debt burdens remain structurally high, with limited political appetite for fiscal austerity. At the same time, spending pressures are unlikely to ease: defense spending is rising alongside geopolitical tensions, while social assistance programs continue to expand across most developed economies.

Layered on top of this is the global investment race in AI — a multi-year capital expenditure and infrastructure cycle spanning semiconductors, energy, data centers, and related supply chains.

The implication is that policymakers are likely to continue tolerating — and in many cases preferring — a regime of financial repression, where the real value of debt erodes gradually over time through inflation and negative real rates. Historically, this backdrop has been supportive for real assets and equities.

But near-term risks are not trivial

A supportive long-term backdrop does not guarantee smooth returns. Cyclical pullbacks of 10–20% can and likely will occur along the way.

One concern is market structure. Leverage and speculative positioning tend to rise when financial conditions are loose, and margin debt currently sits near record levels. In an environment where policymakers are biased toward lower interest rates, there is a risk that asset prices overshoot and become increasingly unstable.

In that scenario, the sequence is familiar: a volatility shock leads to forced selling, margin calls accelerate the move, and deleveraging creates an “air pocket” in pricing. Market history offers several examples of how quickly this can unfold. This remains one of the greatest risks in the market today.

What would support another leg higher?

For this bull market to extend in a healthier way, the key is breadth — a broader set of stocks participating in gains. A period of consolidation would also be constructive, helping to work off some of the more speculative positioning and allowing margin debt and leverage to moderate.

Two conditions matter most:

- High beta leadership needs to cool while quality and lower volatility catch up.

The high beta versus low volatility ratio is stretched. While it is not uncommon for high beta stocks to lead coming off a market bottom — as we saw following the Liberation Day sell-off — the magnitude and persistence of this move are unusual.

A more sustainable rally would involve leadership broadening toward higher-quality companies with strong balance sheets and durable cash flows, rather than continued multiple expansion in the most speculative areas of the market. A consolidation phase that shakes out excess risk-taking would help reset this relationship.

- Small Caps need to participate.

Small Caps continue to trade as though economic growth is about to roll over. If the economy remains resilient and financial conditions ease, the Small Cap versus Large Cap relationship has room to mean-revert. Historically, market advances tend to strengthen when smaller companies begin to participate.

Several factors could support this shift: lower interest rates that benefit the broader economy, trends toward deglobalization that favor more domestically focused small and mid-cap companies and increasingly stretched valuations among large-cap stocks that encourage rotation into smaller names.

Early signs

It is still early in the year, but initial signs suggest market participation may be improving. If this trend continues, it would represent a meaningful shift away from the concentrated leadership that has defined much of the recent rally toward a broader, more durable market advance.

Part of this broadening in leadership will likely be driven by the AI trade expanding beyond mega-cap hyperscalers and into the broader economy, as other industries begin to realize the benefits of AI-driven productivity gains. This transition, however, is unlikely to be seamless. It will not occur overnight and will likely involve short-term disruptions, particularly within the labour market. While AI productivity should support corporate earnings and profit margins over time, it may simultaneously create macroeconomic headwinds through worker displacement and periods of adjustment.

At Q Wealth, our focus remains on building diversified, factor-aware portfolios designed to perform across different market environments, helping clients participate in long-term growth while managing risk through inevitable market cycles.

Disclosure:

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.