The year came and went, but it was anything but uneventful. Following two consecutive years of returns exceeding 20% in the S&P 500 Composite, our expectation entering 2025 was for more moderate outcomes — high single-digit to low double-digit returns — as markets transitioned away from a liquidity-driven rebound toward a more fundamental phase. While we were not far off, the S&P 500 Composite ultimately finished the year up 17.9% year-over-year on a total return basis. Given the headwinds markets faced — including the Liberation Day–related sell-off in April, the longest U.S. government shutdown on record, and inflation that moderated but remained persistent — we are somewhat surprised by where equity markets sit today.

We should be clear that our process is not built around forecasting short-term market outcomes. We are not in the prediction business; rather, our focus is on constructing portfolios that are resilient across a wide range of market environments. That said, we will chalk up the past year as a positive outcome relative to our expectations, particularly given the magnitude of the challenges markets faced. We have also been consistent in our view that we remain in a secular bull market. However, for any bull market to be durable, periods of consolidation are not only inevitable but healthy. Earnings ultimately need time to catch up with prices, and equity multiples cannot expand indefinitely.

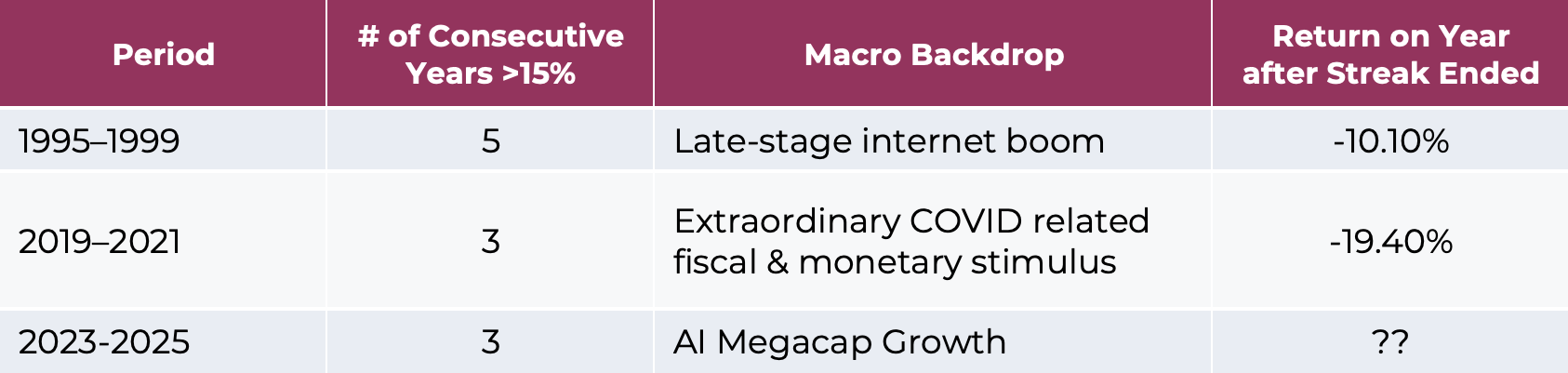

History reinforces this point. Since 1927, the S&P 500 Composite (including predecessor indices) has delivered three or more consecutive calendar years of returns exceeding 15% on only two other occasions: during the late-stage dot-com expansion from 1995 to 2000, and during the liquidity-driven COVID period from 2019 to 2021, the latter fueled by an unprecedented combination of fiscal and monetary stimulus. While history never repeats perfectly, it serves as a reminder that extended periods of outsized returns are typically followed by phases of consolidation or normalization, rather than uninterrupted gains. This is not a near-term forecast; however, recent performance has been highly concentrated within a narrow group of AI-exposed mega-cap companies, implying that sustained index-level returns will ultimately depend on a broader diffusion of AI-driven productivity gains and/or a more accommodative monetary backdrop, rather than continued mega-cap leadership alone.

Will the Run in the S&P 500 Composite Continue?

Source: Bloomberg, using data on S&P 500 Composite (and predecessor indices) back to 1927

Key Themes to Watch in the Year Ahead

It is against this backdrop — resilient markets and elevated expectations — that we turn our focus to the key themes we believe will shape markets in the year ahead and beyond. Rather than attempting to forecast precise outcomes, our emphasis remains on identifying the forces most likely to influence return dispersion, volatility, and portfolio construction.

- AI Broadening Beyond Mega-Caps

AI leadership is beginning to broaden beyond a narrow group of mega-cap beneficiaries. While this should support productivity across more industries over time, the transition may be choppy as competition intensifies. - Federal Reserve Leadership and Independence

The next Federal Reserve Chair could meaningfully influence markets in both the short and long term. Preserving Federal Reserve independence remains critical to policy credibility and long-term market stability. - Interest Rate Policy and Political Pressure

Interest rates will remain a key market driver, shaped by inflation dynamics, structural fiscal pressures, and the political cycle. Markets are likely to be sensitive not just to rate direction, but to perceived policy constraints. - Cyclical Risks Remain Despite Secular Bull-Market

While we believe the market remains in a long-term secular bull, cyclical risks persist. Political, systemic, and geopolitical factors continue to create the potential for periodic volatility.

1) AI Diffusion: Next Up, AI Benefactors

The AI narrative is entering its next phase. After an initial period of highly concentrated market leadership, we believe AI adoption is beginning to broaden across sectors and industries. As highlighted in our recent blog on AI and market breadth, this shift reflects a transition from speculative enthusiasm toward practical implementation. Increased competition among large platforms is accelerating this evolution. Players such as Google, which control the full AI technology stack — from proprietary chips and infrastructure to models, distribution, and balance sheet strength — are exerting downward pressure on pricing across the ecosystem. While this dynamic should lower costs and expand access to AI capabilities, it also raises the risk of margin compression for many first-order AI providers.

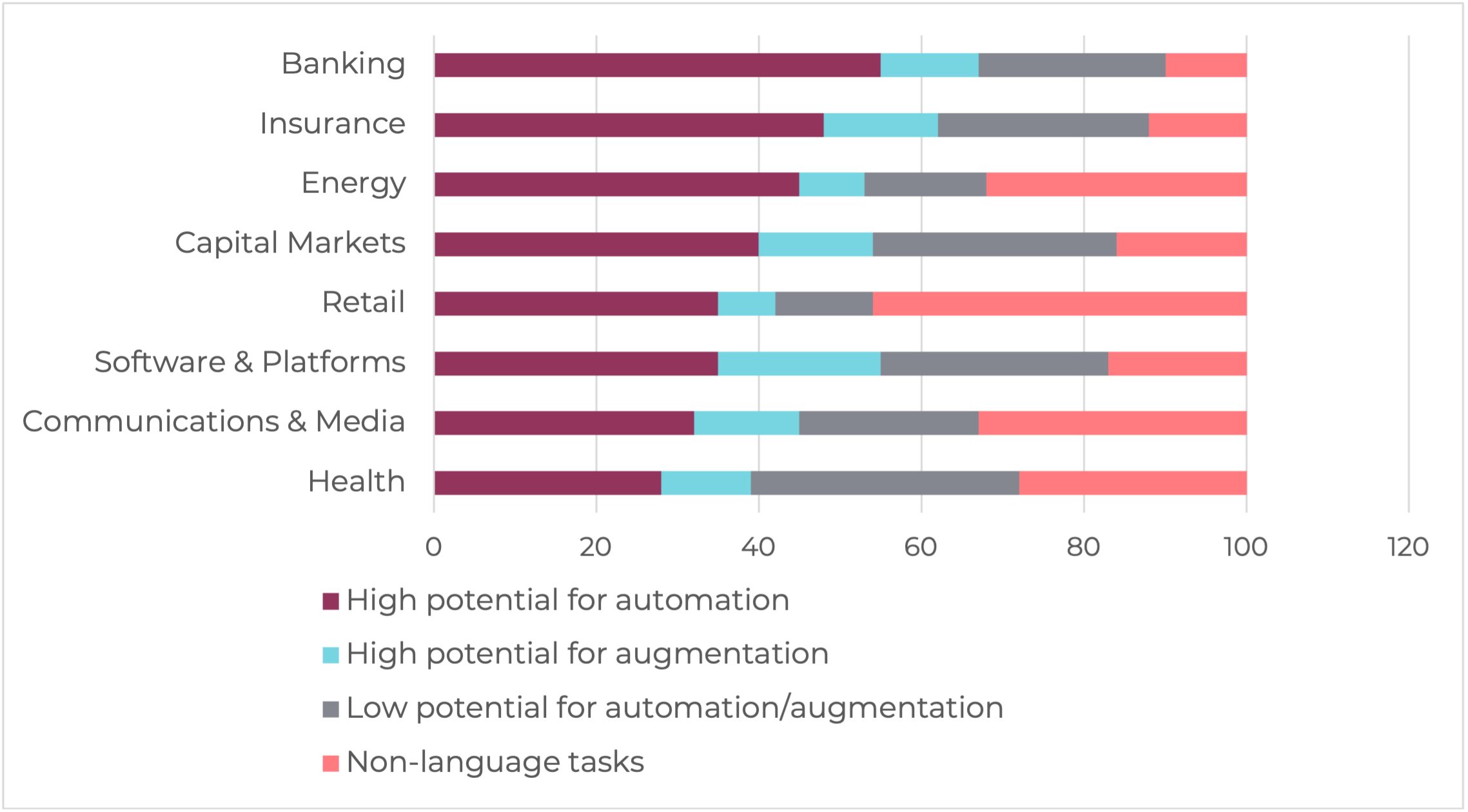

In this environment, we believe the economic benefits of AI are increasingly likely to accrue to second-derivative beneficiaries: companies that apply AI to enhance productivity, efficiency, and decision-making rather than those focused solely on building foundational models. Industrials, healthcare, financial services, logistics, and enterprise software stand to benefit as AI becomes embedded into existing workflows. While this evolution should support longer-term earnings growth and broader market participation, the transition is unlikely to be linear. As leadership rotates and expectations reset, periods of volatility are likely. Moreover, the pace of adoption may prove uneven, benefiting companies that successfully integrate AI while displacing those unable to adapt. While AI is likely to be supportive of corporate profit margins over the long run, the pace of labor displacement it introduces may create near-term macroeconomic frictions as economies adjust.

Anticipated Share of Working Hours that Can be Replaced by AI

Source: Accenture/Statista (Share of working hours in selected industries in the U.S. that could be automated/augmented by the use of AI)

2) Federal Reserve Leadership Transition: Why It Matters for Markets

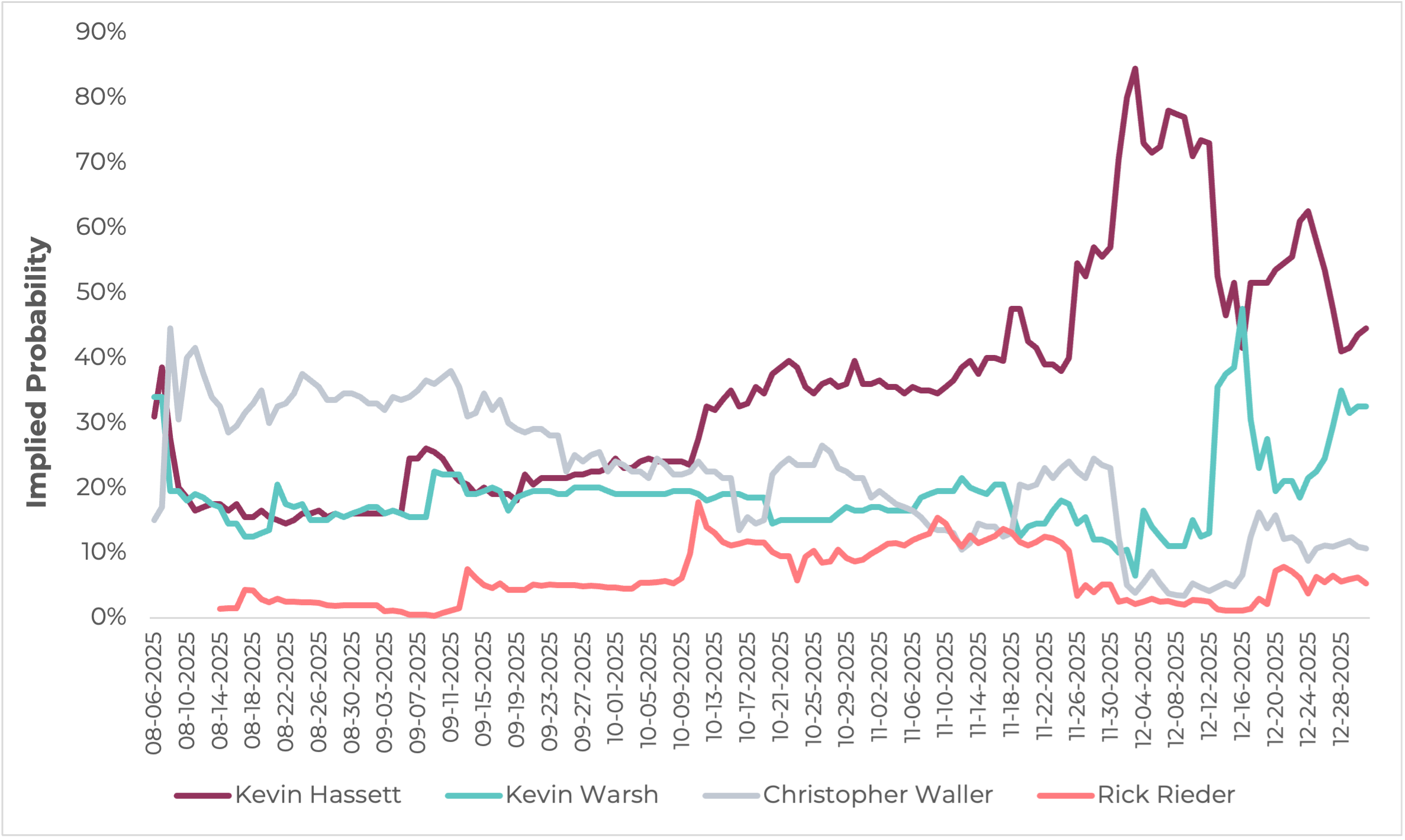

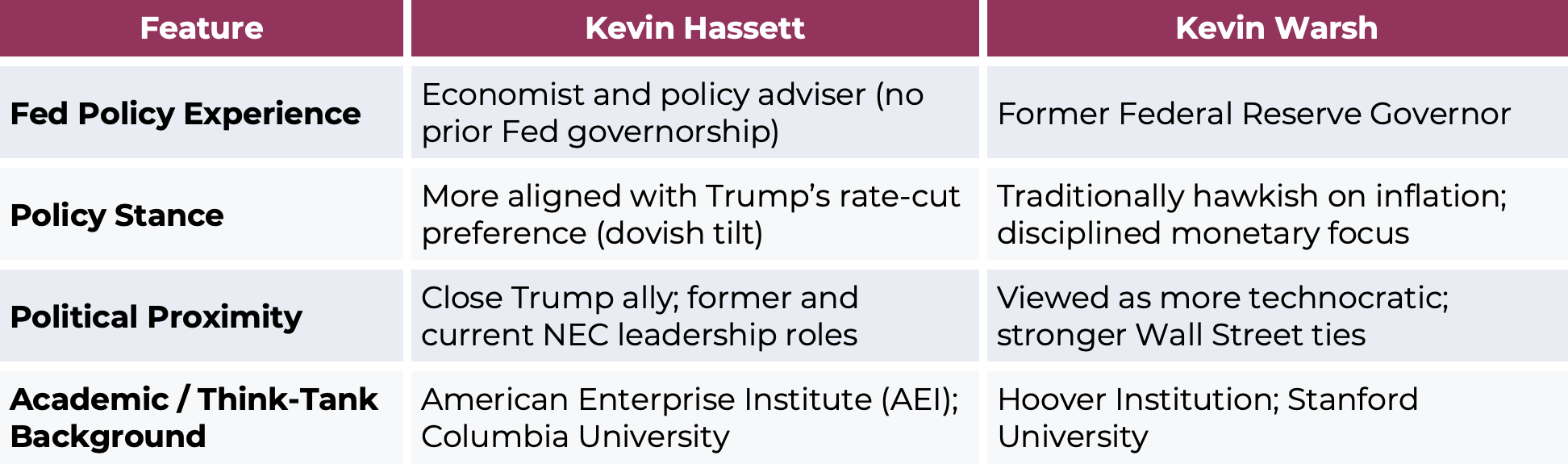

With Chair Powell’s term set to end in May 2026, a Federal Reserve leadership transition is increasingly coming into focus. A continuation of Powell’s tenure appears unlikely, given President Trump’s repeated and public criticism of the current Fed Chair. As a result, markets are beginning to assess not only the future path of interest rates, but also the policy philosophy and credibility of the next Federal Reserve leadership. According to Polymarket, the race is currently close between Kevin Hassett and Kevin Warsh, with Warsh recently gaining momentum following public support from Jamie Dimon. While we believe currency debasement is inevitable over the long run given the unsustainable debt-to-GDP trajectory of the U.S. government, the selection of the next Fed Chair could meaningfully influence the short- and medium-term performance of risk assets, reflecting differences in policy approach, communication style, and perceived independence.

Who Will be the Next Fed Chair?

Source: Polymarket.com (as of December 31, 2025)

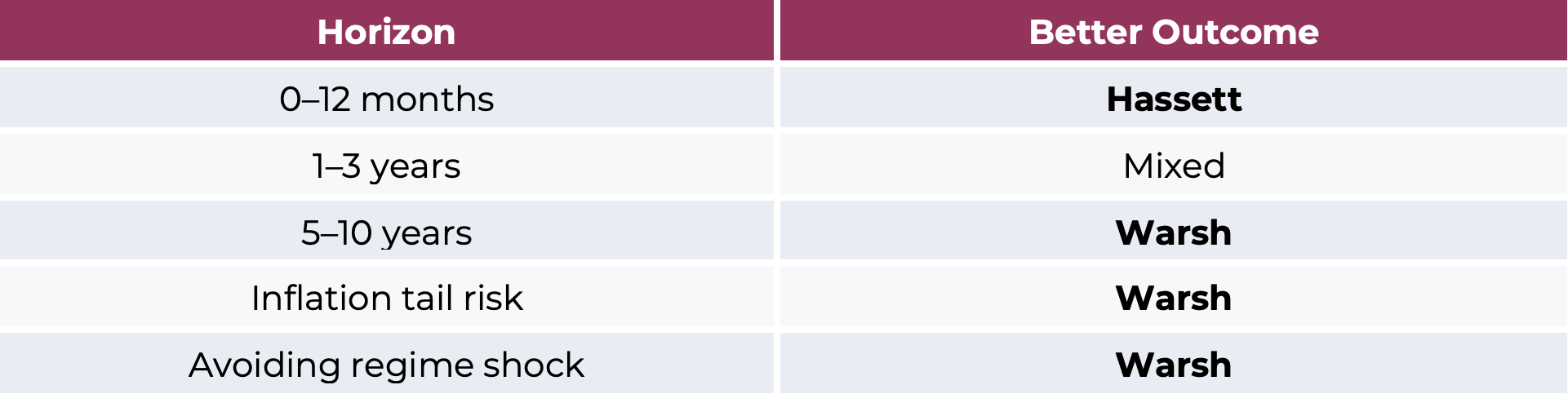

Although both candidates would operate under the same macro-economic constraints, their approaches to inflation tolerance, rate policy, and institutional credibility could produce very different market outcomes during the next phase of the cycle.

The durability of a secular equity bull market in 2026 and beyond depends less on short-term stimulus and more on the perception of Federal Reserve independence and inflation credibility. Equity multiples do not require very low inflation; they require stable and predictable inflation. A regime in which inflation is contained below roughly 3.5%, with limited volatility, can support both sustained earnings growth and multiple expansion. Markets tend to reward policy frameworks that anchor expectations and minimize inflation tail risks, even if policy is not overtly easy. Credibility lowers the equity risk premium, stabilizes discount rates, and supports more durable valuation expansion. In this context, the key risk for markets is not higher interest rates per se, but a loss of confidence in the policy framework that could ultimately force more abrupt tightening. The most constructive backdrop for equities remains one of managed debasement — modestly higher trend inflation, credible monetary policy, and financial conditions that support growth without overheating — under which equities should continue to outperform bonds over the long term.

Against this backdrop, Kevin Hassett would likely be more supportive of equity markets in the near term, reflecting his greater comfort with lower interest rates and a higher tolerance for inflation. His closer alignment with the Trump administration increases the likelihood of maintaining easier monetary conditions, which could be positive for risk assets in the short and medium term. However, this same proximity raises the risk of prolonged policy accommodation, increasing the probability that inflation pressures re-accelerate or remain elevated.

By contrast, Kevin Warsh may offer a more durable framework over longer horizons, particularly if preserving the perception of Federal Reserve independence remains a priority. While Warsh’s approach may be less favorable for equity multiple expansion in the short run, effective inflation management improves the odds of sustained multiple expansion over time by lowering inflation tail risk and reinforcing policy credibility. In our view, inflation remains the key variable: Hassett may be better for equities in the short and mid-term, but Warsh is better positioned to support a more stable and durable equity regime over the long run.

3) Debasement as Policy: Credibility, Fiscal Reality, and the AI Arms Race

Against the backdrop of a Federal Reserve leadership transition, the perception of Fed independence becomes increasingly important. Should policy credibility weaken, investors are likely to demand a higher term premium to compensate for greater uncertainty around inflation and policy direction, placing upward pressure on long-term yields. In such an environment, recent history suggests central banks are more inclined to reassert control over the long end of the curve, including renewed Treasury purchases to stabilize market functioning — even if framed as technical or liquidity-driven operations rather than formal quantitative easing. Recent increases in short-dated Treasury purchases, while largely intended to manage bank reserve levels around seasonal corporate tax payments, nonetheless highlight how readily balance-sheet tools can be reintroduced when liquidity conditions tighten, reinforcing the asymmetry of policy responses in a highly leveraged system

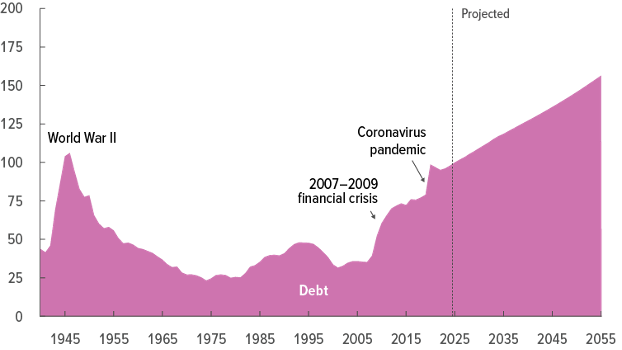

At the same time, the debt-to-GDP challenge continues to grow, with limited political appetite for austerity or meaningful fiscal consolidation. In practice, this leaves policymakers with a narrow set of tools: allow productivity growth to do the heavy lifting where possible — increasingly via AI-driven efficiency gains — while quietly reducing the real burden of debt through managed debasement. Compounding this dynamic is the global race for AI and technological leadership, which all but guarantees sustained government spending on energy, infrastructure, semiconductors, and strategic industries. Deglobalization and national-security considerations further reinforce this fiscal bias, making lower deficits structurally difficult to achieve.

This combination underpins our view that debasement is not a policy choice, but a policy outcome. Over the long run, nominal corporate earnings must expand alongside inflation, supporting a secular bull market for equities, provided inflation remains managed and policy credibility intact. Central banks’ task is to strike this balance — maintaining real rates low enough to erode debt burdens without destabilizing expectations. It is no coincidence that central banks have continued to diversify reserves away from fiat currencies and toward gold, reflecting a desire to hedge long-term currency risk. In addition to equities, we believe this regime favors gold, real assets, and selected digital assets, though the growing adoption of stablecoins may temper Bitcoin’s role as a transactional currency even as it retains appeal as a debasement hedge.

U.S. Debt to GDP Nearing Historic Highs

Source: Congressional Budget Office (CBO) – Long Term Budget Outlook 2025 - 2055

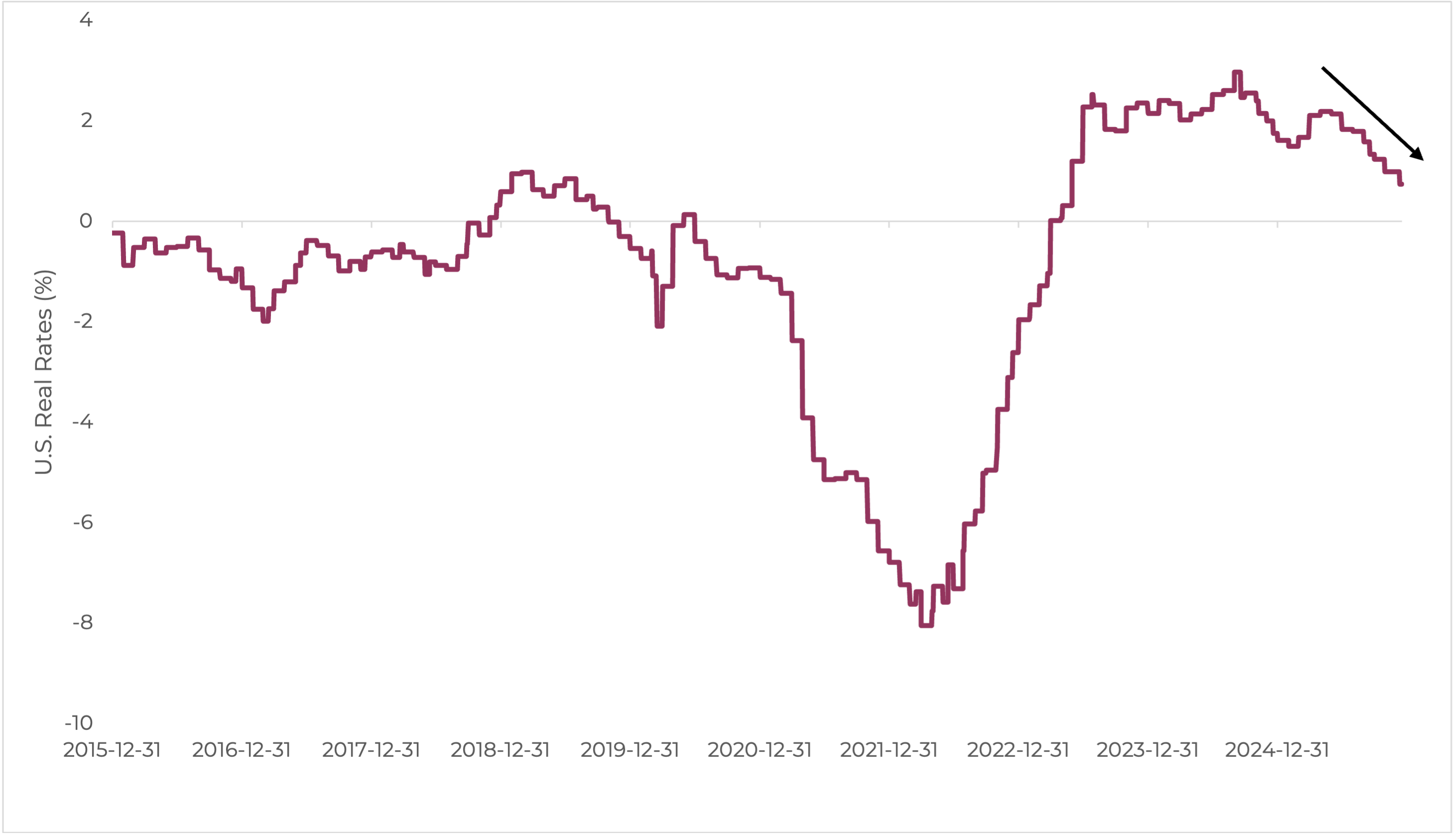

Are U.S. Real Rates Headed Negative Again?

Source: Bloomberg as of December 16 (U.S. Real Rates expressed as difference between U.S. CPI -Y/Y and Federal Funds Target Rate – Upper Bound)

4) Risks on the Horizon: Secular Bull Market, Rising Cyclical Fragility

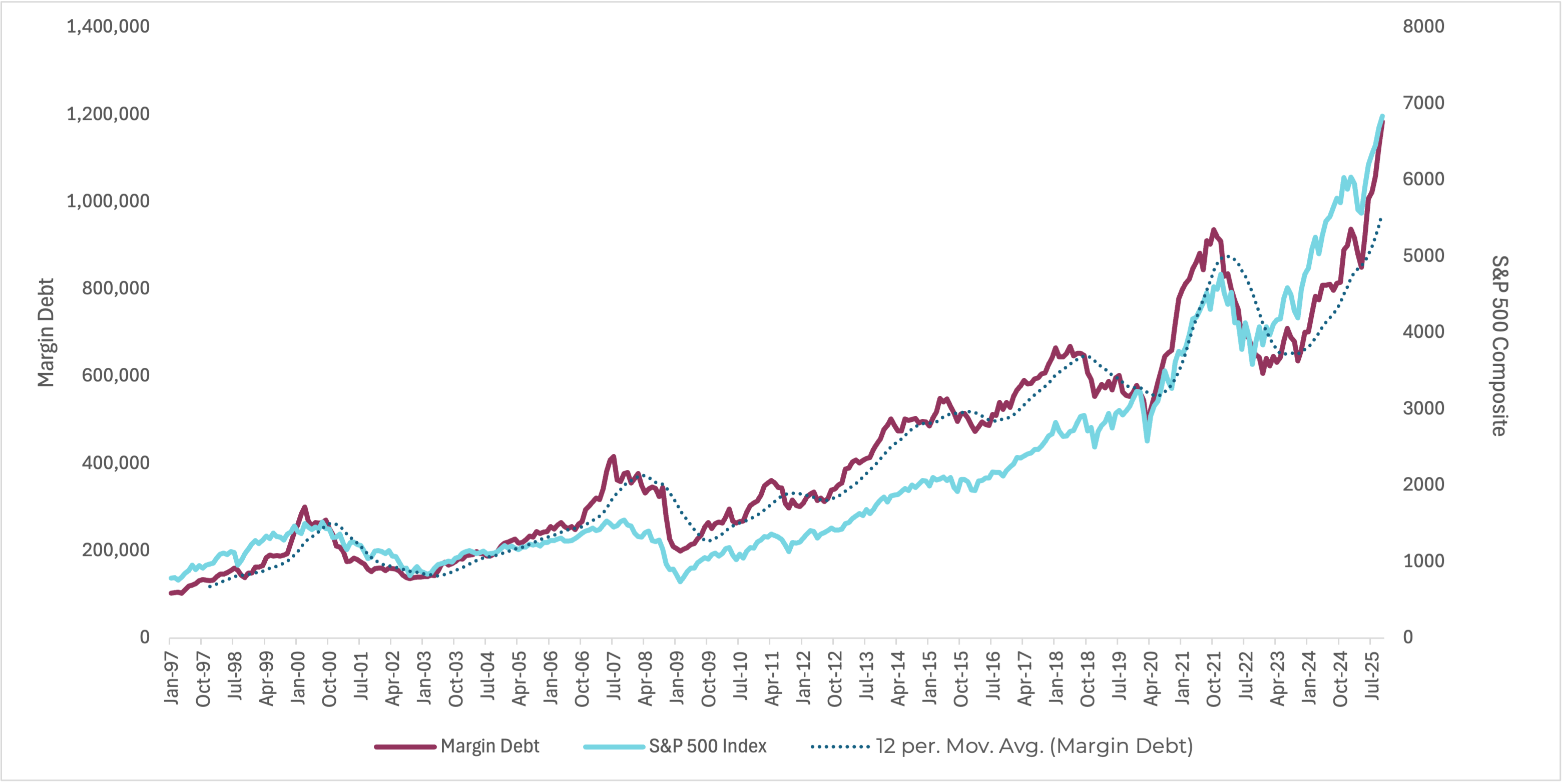

While we believe the debasement regime supports a long-term secular bull market, this does not preclude the occurrence of cyclical bear markets. In fact, systemic risks appear to be rising. Higher yields can introduce nonlinear shocks into leveraged parts of the financial system, as seen in 2022 with long-duration UK gilt exposures within pension funds and the rapid repricing of U.S. regional banks’ held-to-maturity portfolios. Today, margin debt levels sit near all-time highs, increasing the sensitivity of markets to drawdowns. Should risk assets decline beyond a critical threshold, margin calls can force rapid deleveraging and forced selling, amplifying market moves and triggering broader stress through liquidity events, policy missteps, or exogenous shocks — not solely through a traditional economic recession.

Geopolitical risks are also increasing, albeit in a more complex and less binary form. While the current U.S. administration has been effective in de-escalating active conflicts in the Middle East and has made progress toward a negotiated outcome in Russia–Ukraine, geopolitical tension is increasingly shifting toward strategic competition, particularly around AI supremacy. Rivalry between major powers — most notably the U.S. and China — is intensifying in areas such as energy security, advanced manufacturing, and access to critical inputs including rare earths and semiconductors, raising the risk of episodic volatility even in the absence of outright military conflict.

Finally, we continue to see a deeper shift toward deglobalization, characterized less by isolation and more by the formation of strategic economic blocs. As geopolitical competition intensifies, global integration is increasingly giving way to selective cooperation within aligned alliances, while tariffs, industrial policy, and national security considerations play a greater role in directing capital flows. This bloc-based world reduces the efficiency of a single global system and constrains the free flow of capital across regions, increasing dispersion between countries, sectors, and asset classes. As a result, portfolio construction matters more than it has in prior cycles — not only from an asset allocation perspective, but also in terms of regional exposure, supply-chain alignment, and geopolitical resilience.

Margin Debt Exposes Markets to Higher Velocity Drawdowns

Source: FINRA, Bloomberg

Conclusion: Ushering in 2026

While we believe the current environment supports a long-term secular bull market, this does not allow for a complacent investment approach or a strategy that simply remains long equities while ignoring risk. Cyclical pull-backs can and will occur. The global macroeconomic backdrop has become more complex, with policy transitions, geopolitical competition, and higher leverage increasing both the frequency and magnitude of market volatility. As a result, portfolio construction must be more sophisticated than ever, balancing participation in long-term growth with resilience to cyclical dislocations.

The durability of this secular bull market ultimately hinges on the Federal Reserve’s ability to maintain credibility while managing a gradual debasement of the currency without destabilizing inflation expectations. While this framework can support asset prices over time, it does not eliminate near-term risks. As outlined throughout this outlook, a range of side narratives — from deleveraging events to geopolitical and policy shocks — can introduce meaningful volatility along the way.

In this environment, a well-constructed portfolio is designed to absorb both short-term noise and long-term regime shifts. This requires thoughtful diversification across factors, asset classes, regions, and liquidity profiles — ensuring portfolios can both draw on liquidity when needed and maintain exposure to less liquid assets that support long-term return objectives. As we head into 2026, we remain optimistic about the opportunities ahead, while staying focused on strategic growth, disciplined risk management, and meaningful downside protection aligned with our clients’ liquidity and long-term goals.

Disclosure:

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.