The market continues to push to new highs, but the underlying structure is far more nuanced than the headline numbers imply. Market breadth remains narrow, leadership is concentrated almost entirely in AI-linked mega-caps, and the S&P 500 Equal Weight Index continues to lag the cap-weighted S&P 500 Composite by one of the widest margins on record. This divergence underscores a key reality of the current environment: a small group of companies is doing most of the heavy lifting.

None of this suggests the secular bull market is over. If anything, a period of consolidation would be healthy for the long-term sustainability of the cycle, allowing prices to realign with earnings and giving the next leg of leadership time to form. AI is clearly transformative — arguably an industrial revolution in its own right — with the potential to scale productivity and contribute powerful disinflationary forces at a time when fiscal expansion remains elevated. We continue to believe that markets are in a multi-decade secular uptrend. But secular trends do not move in straight lines. They are punctuated by cyclical pullbacks, pauses, and leadership rotations — particularly when valuations become top-heavy and expectations increasingly ambitious.

Today’s environment checks many of those boxes.

Market Breadth Remains Narrow: SPX vs. SPX Equal Weight Divergence

One of the simplest ways to assess market breadth is by comparing the cap-weighted S&P 500 Composite with the S&P 500 Equal Weight Index. It currently implies that:

- The average stock has not kept pace with the index

- A small group of mega-cap companies are responsible for the majority of gains

- The divergence between cap-weighted and equal-weighted S&P 500 is the widest since August 2010

S&P 500 Composite has Diverged from S&P 500 Equally Weighted

Supporting this, only 51.8% of S&P 500 constituents are above their 50-day moving average. While there is no single threshold that defines a healthy bull market, periods of durable strength typically see 60% or more of stocks participating. Beneath the surface, participation varies significantly by sector:

% of Stocks Above 50-Day Moving Average (Sector Level)

- Energy: 86%

- Health Care: 72%

- Consumer Staples: 62%

- Information Technology: 39%

- Utilities: 23%

The takeaway:

The S&P 500 is rising, but the market is not rising with it. Breadth remains narrow, and while technology stocks have been weak on a participation basis, their mega-cap dominance continues to lift the index, masking underlying fragility.

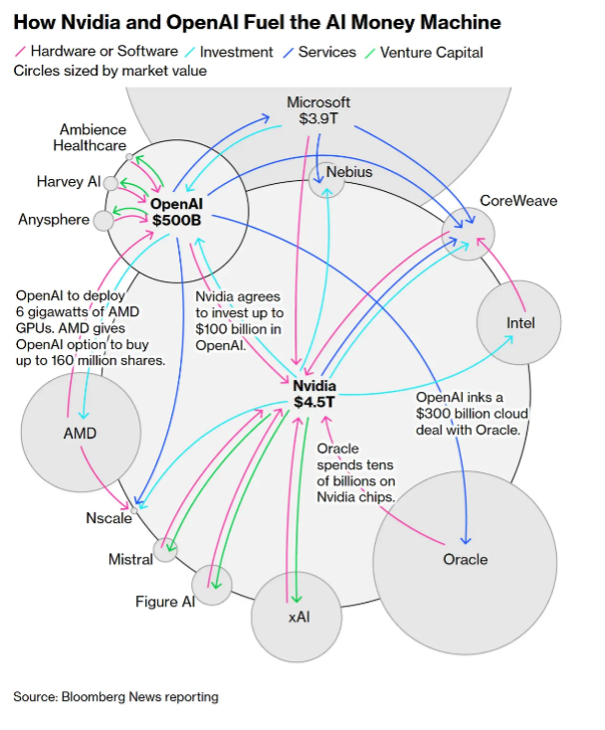

AI Has Become the Market’s Center of Gravity — But Circular Capex Concerns Are Rising

While today’s AI leaders (NVIDIA, Microsoft, Meta, Google) are nothing like the speculative companies of the late 1990s—with real earnings, deep cash flow, and dominant competitive moats—the structure and pace of the current AI investment cycle is creating new questions around sustainability.

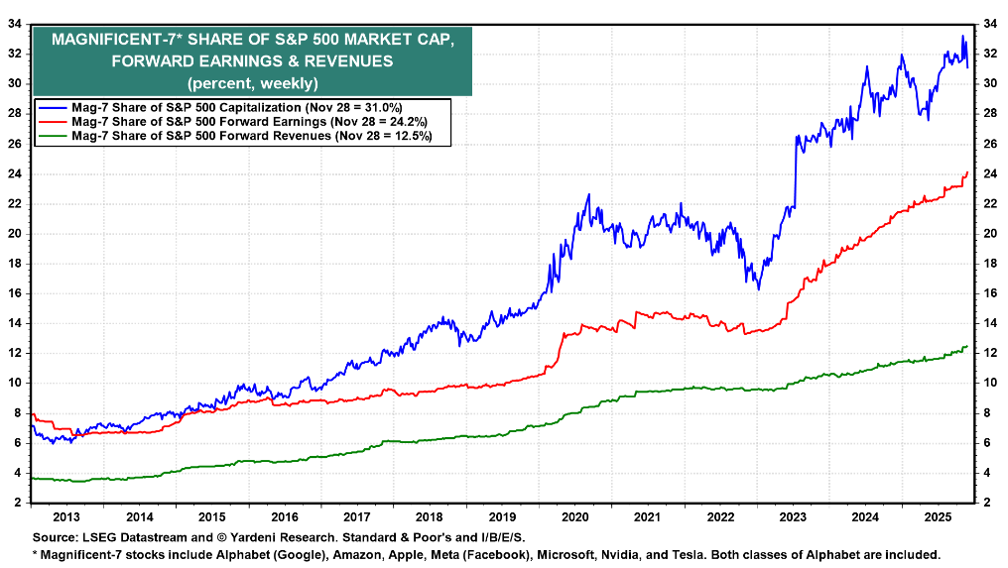

The Magnificent 7 now account for:

- 31% of S&P 500 market cap

- 24% of index earnings

- 12.5% of revenues

And almost all of the S&P 500’s margin expansion over the past two years has come from this small group—driven heavily by AI-linked capex intensity and the profitability of the AI supply chain.

What is increasingly debated is the circular nature of AI spending, where hyper-scalers, model developers, chip providers, and cloud operators simultaneously drive each other’s revenues and capital commitments. This feedback loop is extremely powerful in an upcycle—but it can become fragile if monetization slows or if competitive dynamics begin to pressure pricing.

A good illustration of these growing concerns: Oracle’s 5-year CDS spreads have risen sharply. This does not imply Oracle is at risk of default; instead, it signals that credit markets are beginning to price in the balance-sheet strain associated with large-scale AI infrastructure spending across the ecosystem.

Importantly, we do not view this as a bubble. The AI leaders are profitable, entrenched, and central to enterprise technology. But just as the long-term winners of the internet era extended far beyond pure dot-com companies, we expect the next phase of AI to broaden—where industrials, healthcare, financials, and other adopters begin to capture meaningful productivity gains.

This broadening is both healthy and necessary for the durability of the secular bull market. And for long-term investors, the opportunity often emerges before new leadership is fully recognized—when the beneficiaries are still underappreciated.

5-Year CDS on Oracle Have Surged Higher

Market Dominance Always Attracts Competition — And NVIDIA Is No Exception

NVIDIA has been the clear winner of the AI buildout, effectively becoming the chip provider to the entire ecosystem. Its dominance — and the extraordinary margins that come with it — were never going to go unchallenged. As in every industry, high profitability eventually draws credible competition.

Enter Alphabet/Google.

Google is uniquely positioned to pressure the economics of the current AI supply chain because it controls more of the capital stack than any other player:

- Its own custom silicon (TPUs)

- Its own global data-center network

- Its own frontier models (Gemini)

- Its own consumer and enterprise distribution across Search, Android, YouTube, and Workspace

- And critically — the ability to price AI at or near cost by virtue of vertical integration

Meta’s decision to begin adopting Google TPUs is a meaningful signal that this competitive phase has begun.

If Google leans further into price-based competition, it could:

- Compress model-training and inference margins

- Create headwinds for hyper-scaler profitability

- Slow the circular capex loop that has fueled recent earnings

- And ultimately impact Mag-7 earnings expectations, given how dependent they have become on AI-linked margin expansion

This does not derail the long-term AI secular trend. Instead, it signals a natural evolution: the shift from early-cycle hypergrowth driven by a single dominant supplier (NVIDIA) to a more competitive, mature phase where efficiency, pricing power, and adoption across the broader economy begin to drive the next leg of returns.

Portfolio Implications: Diversify With the Index, Not Away From It

We are not advocating selling out of index exposure. The S&P 500 has been — and will continue to be — one of the most powerful long-term wealth-building tools available to investors. But when concentration reaches historical extremes, it becomes prudent to complement passive exposure with strategies that help balance risk, broaden participation, and capture the next phase of market leadership.

In other words, this is not about abandoning beta — it’s about improving the resiliency of the portfolio around it.

Factor Strategies (Quality, Low Volatility, Size, Dividend Growth)

Factor investing offers exposure that aligns well with today’s market structure:

- You still maintain exposure to the Mag-7, especially through Quality, which tends to overweight profitable, dominant blue-chip companies.

- You gain diversified exposure to durable non-AI blue chips, which can participate as AI-driven productivity spreads through the broader economy.

- Factors provide a better balance between cyclicals and defensives, reducing reliance on a single market narrative.

- Concentration risk declines, helping mitigate drawdowns should mega-cap leadership pause or rotate.

- Low Volatility and Quality historically outperform during periods of narrow breadth and elevated dispersion — precisely the environment we are in today.

These strategies don’t compete with the index — they complement it.

Active Strategies

When used deliberately, active management can play a meaningful role in navigating this backdrop:

- Reduce dependence on a small cluster of mega-caps that dominate passive indices.

- Identify companies benefiting from AI productivity gains, not just AI infrastructure spending.

- Tilt toward areas the equal-weight index may miss, including structural compounders or emerging leaders outside the top-7.

- Adapt more efficiently to sector rotations, especially if breadth begins to broaden.

We favour active managers who are willing to look different from the benchmark, rather than closet indexers. Properly implemented, active strategies can diversify portfolio drivers without sacrificing long-term return potential. Importantly, we are not referring to all active managers, but to those with true alpha potential — managers with high-conviction positioning, disciplined risk controls, and differentiated research processes. These need to be curated carefully. When selected appropriately, these approaches can complement index exposure far more effectively than simply equal-weighting index constituents, while still allowing investors to participate fully in the long-term secular growth of the market.

And to be clear: this is not a criticism of indexing. As one of Canada’s largest index portfolio managers in a previous life, I remain a strong believer in its long-term effectiveness. But when concentration climbs to multi-decade highs, taking some gains off the table and reallocating to complementary exposures becomes prudent risk management — not a market call.

Conclusion: A Narrow Market Today, A Healthier Market Tomorrow

We remain long-term secular bulls, yet cyclical pull backs can and will occur.

AI is a genuine technological revolution, not a hype cycle. The companies building AI infrastructure will continue to matter — but the companies using AI will increasingly drive the next phase of the bull market.

Today’s narrow leadership is not a warning sign. It’s a transition phase.

And like every transition phase in every secular bull market:

- A pullback can be healthy

- Leadership can rotate

- Breadth can improve

- Productivity gains can broaden

- The next leg of the cycle can emerge stronger than the last

Staying diversified, being thoughtful about exposures, and recognizing where expectations are elevated — that’s how investors can not only participate in the secular bull market, but thrive within it.

Disclosure:

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.