When Did the Strike Occur?

On February 28, 2026, the United States and Israel launched coordinated air and missile strikes on Iranian military targets. The action marked a significant escalation in tensions that had been building for months.

Iran confirmed that Supreme Leader Ayatollah Ali Khamenei was killed in the strikes, materially increasing regional uncertainty.

Why Did It Happen?

Officials framed the operation around three primary objectives:

- Targeting Iran’s nuclear, missile, and military infrastructure

- Reducing perceived threats to U.S. forces and regional allies

- Responding to escalating regional proxy activity

Diplomatic efforts earlier this year failed to produce a resolution, and tensions intensified in the weeks preceding the strike.

While Iran’s domestic unrest formed part of the broader backdrop, the stated justification focused on security and strategic deterrence — not regime change.

How Did It Unfold?

U.S. and Israeli forces conducted coordinated strikes on military and strategic targets.

Iran has since launched retaliatory missile and drone attacks on Israeli territory and U.S. positions in the region, expanding the conflict footprint.

The Strait of Hormuz: Why Markets Care

The Strait of Hormuz is one of the most important economic chokepoints globally.

- Roughly 20% of global oil supply passes through this corridor.

- A significant portion of global LNG exports also transit this route.

- Major Gulf producers depend on it for energy exports.

Oil is priced globally at the margin. Even the risk of disruption can move prices meaningfully.

If the strait is threatened:

- Oil prices rise

- Inflation expectations increase

- Bond yields initially fall on safe-haven demand

- Equities weaken, particularly cyclical sectors

- Volatility increases

This is not simply geopolitical — it is macroeconomic.

At present, markets appear to be pricing elevated risk rather than a sustained structural supply shock. A true escalation would involve prolonged physical disruption to tanker traffic or direct targeting of major energy infrastructure.

An Evolving Situation

This remains a fluid and rapidly developing situation. Early reports can change, and markets continuously reassess probabilities as new information emerges. Uncertainty is typically highest at the outset of geopolitical events, both in terms of duration and economic implications.

Market Impact (Since the Weekend)

As of March 3, 2026:

Source: Bloomberg

Equities

- MSCI World: down -2.2% (USD)

- S&P 500: down -0.89% (USD)

- S&P/TSX Composite: down -1.6%

Markets have repriced geopolitical risk and the potential for energy-driven inflation pressure. Defensive and energy sectors have shown relative resilience.

Bonds

- Canadian 10-Year Yield: up 11.3bps

- U.S. 10-Year Yield: up 12.4bps

Bond markets are balancing flight-to-safety flows against rising energy-related inflation expectations.

Commodities

- Gold: down 3.4%

- Oil (WTI/Brent): up 12.5%

Implied Volatility

- VIX: up 18.7% to 23.6

- MOVE Index: up 5.9% to 77.75

Volatility indicators across both equity and fixed income markets have risen materially, reflecting heightened uncertainty and a faster repricing of risk. We will likely continue to see periods of rapid repricing and elevated intraday volatility, with markets adjusting both to the upside and downside as new information emerges.

Oil has moved most directly in response to Hormuz-related risk premiums, while gold has benefited from safe-haven demand.

While the headline index moves may not appear dramatic on paper, the repricing has occurred quickly, resulting in elevated volatility and significant intraday swings. End-of-day figures often mask the magnitude of these moves beneath the surface.

At this stage, markets are reflecting higher uncertainty and risk premia — not a prolonged global economic downturn.

The Importance of Staying Invested

Geopolitical events often become politically charged. From an investment perspective, discipline matters more than opinion.

Markets reward process, diversification, and time — not reaction.

History consistently shows:

- Geopolitical shocks create short-term volatility

- Strong market rebounds often occur during periods of peak uncertainty

- Attempting to move to cash introduces significant timing risk

- Missing the strongest recovery days can materially reduce long-term returns

Volatility clusters — and so do reversals.

No one can forecast the precise path of this conflict. What we can control is portfolio discipline.

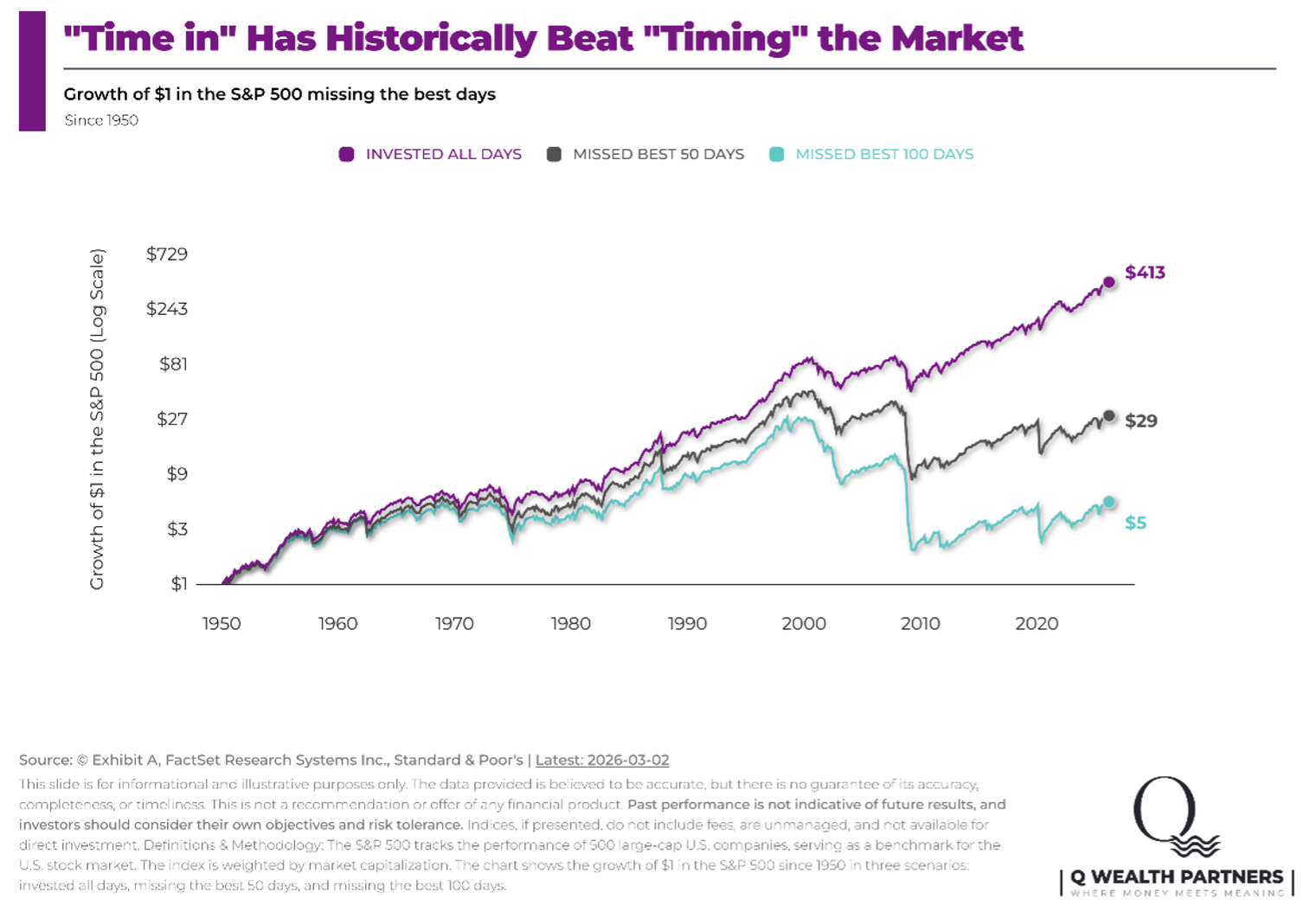

“Time In” the Market Has Historically Beaten “Timing” the Market

Since 1950 (through March 2, 2026):

- $1 invested in the S&P 500 grew to $413 when fully invested.

- Missing the best 50 days reduced that to $29.

- Missing the best 100 days reduced it to $5.

Many of the strongest recovery days occur during periods of heightened volatility — often close to the worst declines.

The cost of being out of the market at the wrong time has historically been far greater than the benefit of attempting to sidestep short-term turbulence.

A Final Thought

Periods like this can feel unsettling. Headlines move quickly, markets react instantly, and uncertainty can dominate the narrative. That is a normal part of investing through global events.

Volatility is not the same as permanent loss. Markets have navigated wars, recessions, political crises, and energy shocks before — and over time, they have continued to advance.

Your portfolio is constructed with diversification, discipline, and long-term objectives at its core. It is designed to absorb uncertainty, not avoid it entirely. Temporary fluctuations are expected; abandoning a sound plan during moments of stress is historically where long-term damage tends to occur.

We will continue to monitor developments carefully and respond thoughtfully if conditions materially change.

If you have questions about how current events relate to your specific portfolio, we encourage you to speak with your QW Advisor. Your strategy is personal, and your advisor can provide guidance tailored to your objectives and circumstances.

Stay disciplined. Stay diversified. Stay invested.

Disclaimer

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The information contained in this document comes from sources we believe to be reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. It is based on various sources, believed to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.

© Quintessence Wealth. All rights reserved.