Following three consecutive years of strong equity returns with the S&P 500 delivering gains in excess of 15% annually, we entered the year expecting a more moderated environment. While markets had demonstrated resilience, the statistical probability of continued outsized returns was becoming increasingly constrained. This was particularly relevant against a backdrop of moderating economic activity, where earnings growth may struggle to keep pace with both price appreciation and elevated expectations.

What was not in our bingo cards, however, was a geopolitical escalation involving Iran — a development that underscores the inherent uncertainty in forecasting market outcomes. Compared to other recent conflicts, tensions involving Iran carry broader implications, not only due to the potential for prolonged engagement, but also because of its proximity to the Strait of Hormuz, a critical chokepoint for global energy supply.

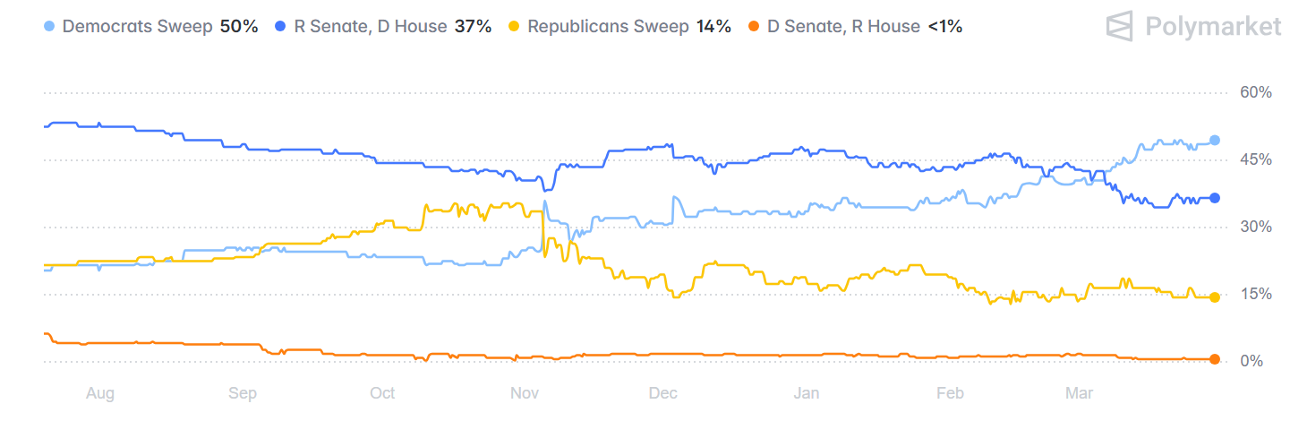

With the U.S. midterm elections on the horizon, the evolving geopolitical backdrop may also carry domestic political implications. While expectations had already pointed to a potential shift in control of the House, prediction markets are increasingly reflecting a broader range of outcomes, including the possibility of changes in the Senate.

Polymarket: A Variety of Outcomes for the U.S. Midterms

Source: Polymarket.com (Balance of Power: 2026 Midterms) as of March 30, 2026

Under the Surface

At Q Wealth Asset Management, we emphasize that we do not attempt to predict markets. This is particularly true in the context of geopolitical events, which are driven by complex strategic considerations, game theory, and incomplete information, dynamics that extend well beyond the scope of financial markets.

Instead, our focus is on understanding how markets behave under different conditions, and on identifying signals within the underlying plumbing of the market that reflect changes in the broader environment.

In recent weeks, several key indicators have begun to shift:

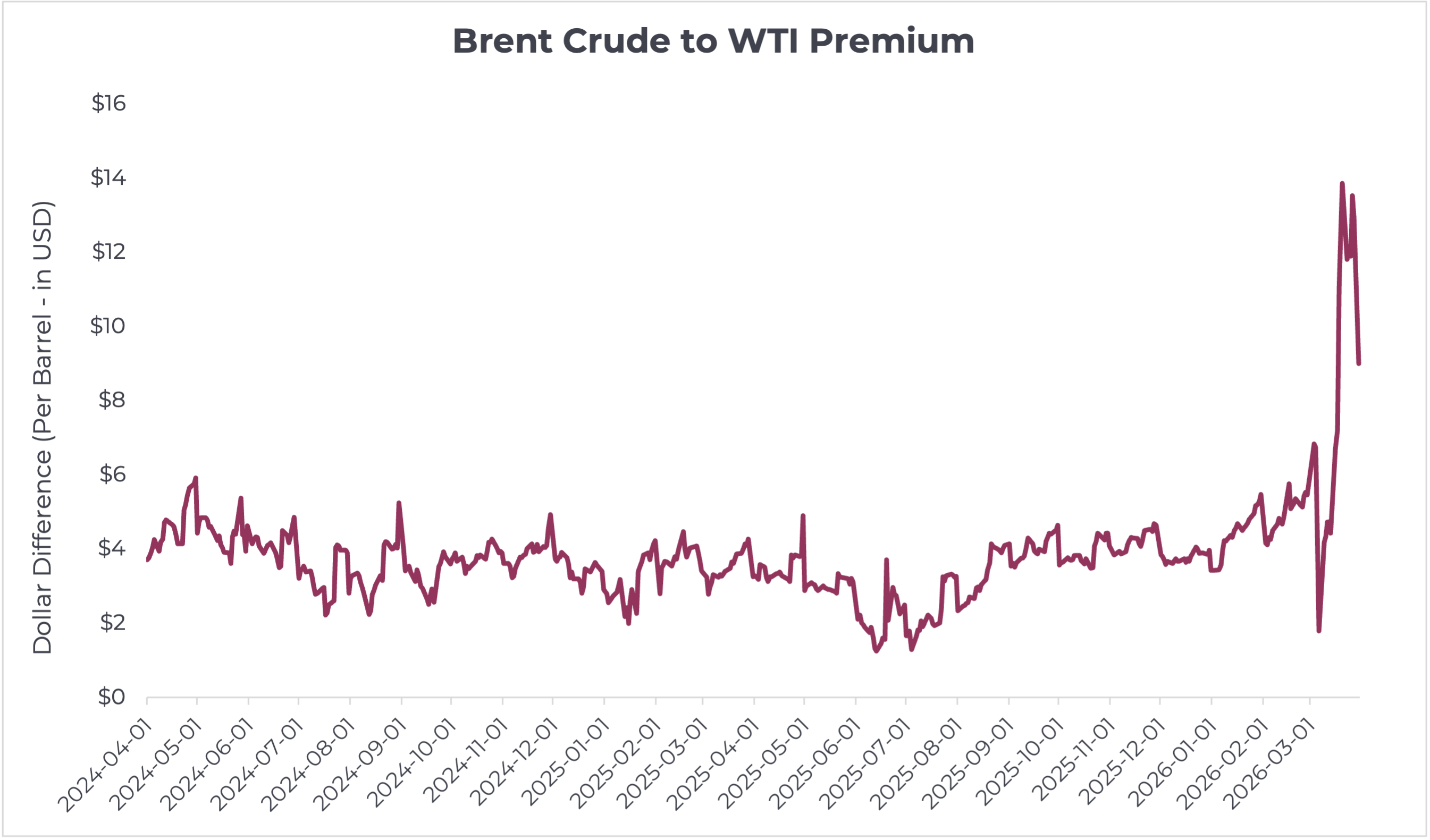

- Oil spreads have widened, pointing to emerging supply-side stress

- Reflects disruption in global energy flows, as Brent crude, the benchmark for global oil, is trading at a premium to WTI, which is more reflective of North American supply

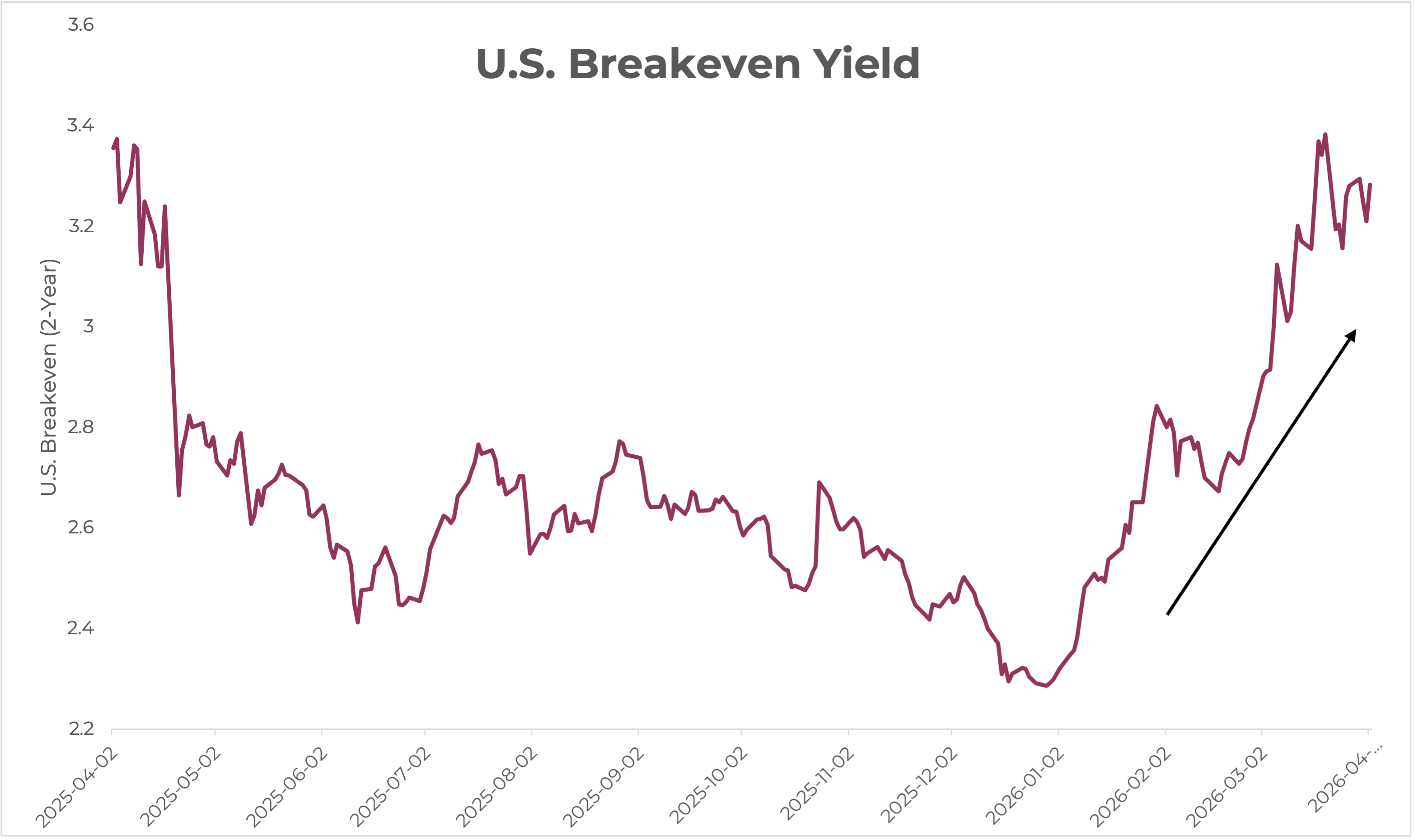

- Breakeven inflation rates have started to move higher

- Suggests that markets are beginning to price in rising inflation expectations, driven in part by higher global energy costs

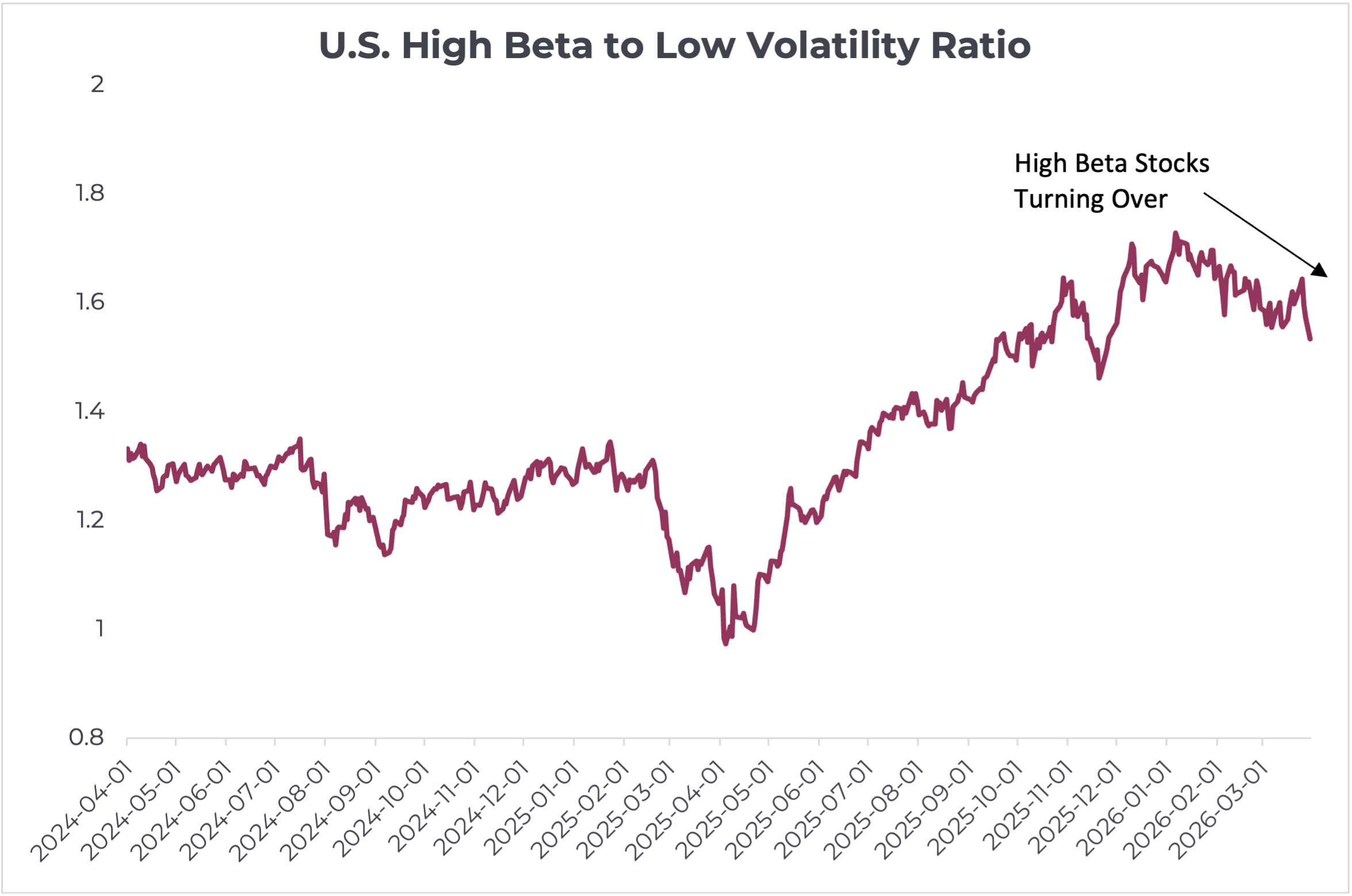

- Equity leadership has started to rotate, with high beta underperforming lower volatility segments

- Indicates early-stage de-risking, as markets begin to favour resilience and balance sheet strength over cyclicality

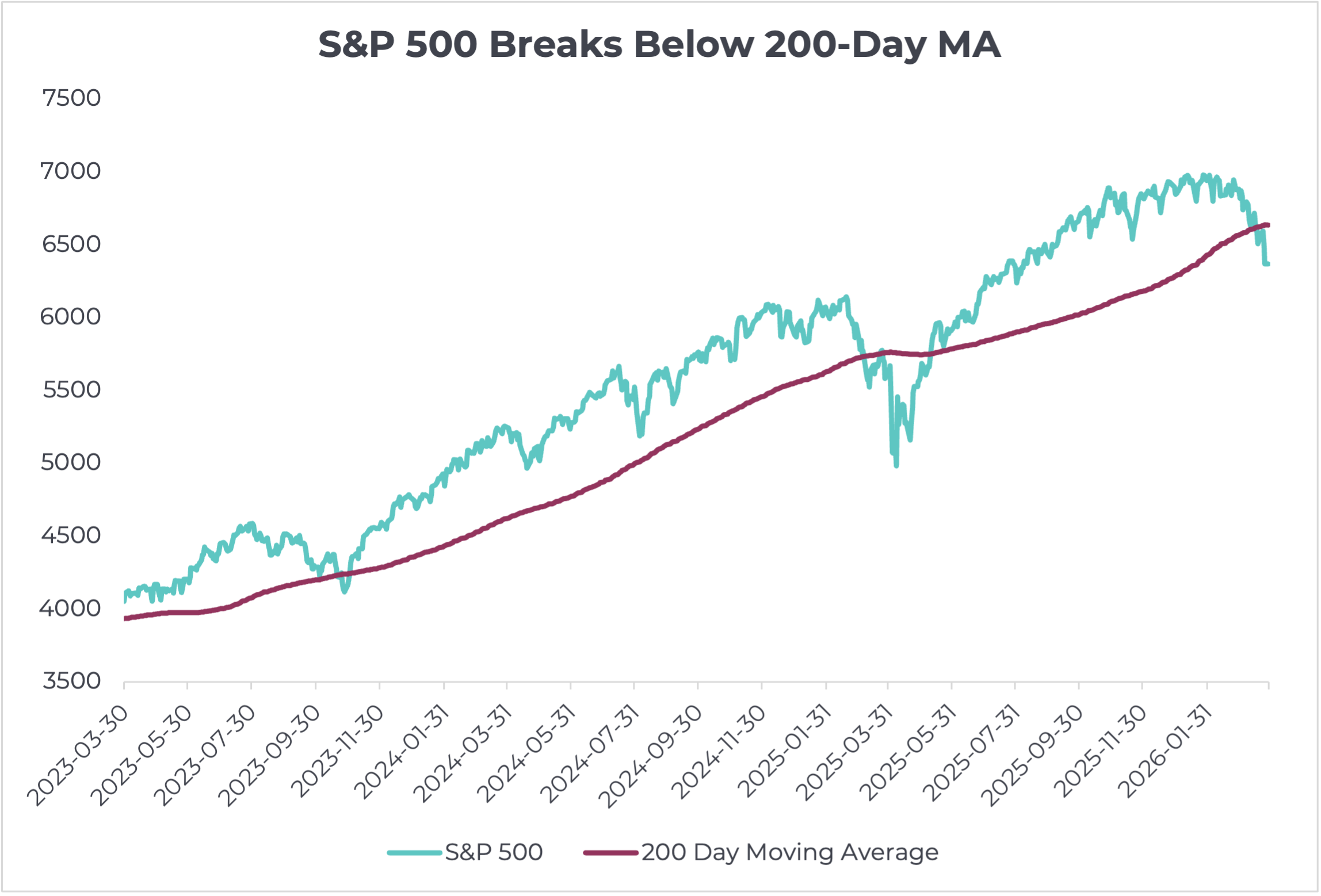

- The S&P 500 has moved below its 200-day moving average, suggesting a deterioration in trend strength

- Points to weakening market momentum and can trigger both systematic and discretionary de-risking

Taken together, these developments suggest that while the catalyst may have been unexpected, the market’s response is consistent with a transition toward a more constrained and less forgiving macro environment — particularly if the conflict continues to drag on.

Alternatively, should President Trump and his administration pursue an off-ramp, or if a ceasefire is reached and disruptions in the Strait of Hormuz are resolved, markets could respond positively. A normalization in energy markets — particularly lower oil prices — would help ease inflationary pressures and potentially allow the U.S. Federal Reserve to resume its path toward monetary easing.

Ultimately, how this geopolitical situation evolves will play a meaningful role in shaping market outcomes through the remainder of the year.

Source: Bloomberg (Spread between front month Brent Crude and WTI contracts, as of March 30, 2026)

Source: Bloomberg (U.S. Breakeven Yield – 2-Year, as of March 30, 2026)

Source: Bloomberg (Ratio of S&P 500 High Beta Index to S&P Low Volatility Index)

Source: Bloomberg (as of March 30, 2026)

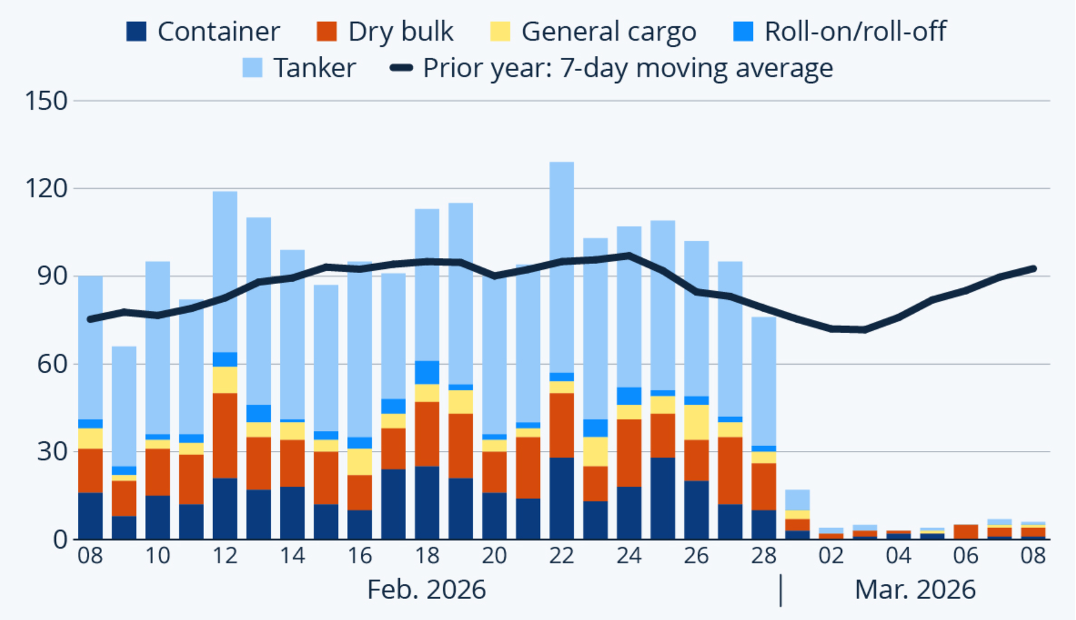

The System Shock: Oil Flow Disruption

The conflict involving Iran has placed the Strait of Hormuz, one of the most critical chokepoints in the global energy system, under pressure. A meaningful portion of the world’s oil supply transits through the region, and recent data shows tanker traffic declining materially from historical norms.

Oil is a foundational input across the global economy, influencing transportation, production, and the broader cost structure of goods and services. As a result, disruptions to its flow act as an initial shock that propagates through markets, contributing to higher inflation expectations, tighter financial conditions, and increased pressure on risk assets.

This is not a market signal — it is a system signal.

Strait of Hormuz Tanker Vessel Crossing

Source: IMF PortWatch, Statista

The Conflict in Iran: Mapping the Range of Outcomes

The evolving conflict involving Iran introduces a wide range of potential outcomes, each with distinct implications for energy markets and the broader macro environment. The duration of the conflict remains uncertain — while the Trump administration may seek an off-ramp, the path to de-escalation can become increasingly complex as engagement deepens, particularly if boots hit the ground.

Across all scenarios, the primary transmission mechanism is oil and its impact on inflation, growth, and financial conditions.

Source: Bloomberg Article GLOBAL INSIGHT: Iran War Endgames - Conflagration to Ceasefire (Written March 18, 2026)

While the range of outcomes is wide, the economic transmission is consistent. Higher-intensity scenarios drive oil prices higher, increasing inflationary pressures and weighing on growth, while de-escalation scenarios primarily act through normalization in energy markets.

Notably, even the most likely outcome, a lower-intensity conflict, implies a persistent geopolitical risk premium in oil, suggesting that the impact may shift from an acute shock to a more sustained headwind for the global economy.

Transmission Mechanism: From Oil to Markets

Oil sits at the center of the global economic system, and movements in energy prices act as a primary transmission channel into broader markets. Rising oil prices increase input costs across the economy, placing pressure on growth while simultaneously lifting inflation expectations. This dynamic contributes to tighter financial conditions, as reflected in higher yields across the curve.

As financial conditions tighten, the cost of credit increases across the economy. Higher borrowing costs reduce disposable income for consumers and raise the cost of capital for businesses, weighing on spending, investment, and overall economic activity. As growth slows, earnings expectations come under pressure, which in turn requires a repricing of risk assets. At the same time, central banks face a more constrained policy environment, while slowing growth would typically warrant easing, elevated inflation limits their ability to do so, as looser financial conditions risk exacerbating price pressures.

In this context, a moderating labour market alongside persistent inflationary pressures raises the risk of a stagflationary environment, one of the more challenging outcomes for both markets and policymakers.

This is the essence of the transmission mechanism: oil drives the shock, and markets adjust through growth, inflation, and financial conditions.

Gold and the Liquidity Paradox

Gold has been one of the strongest performing assets in recent years, supported by a combination of structural factors, including elevated sovereign debt levels, concerns around currency debasement, and ongoing central bank demand. Over the long term, these dynamics continue to provide a strong foundation for gold as a store of value.

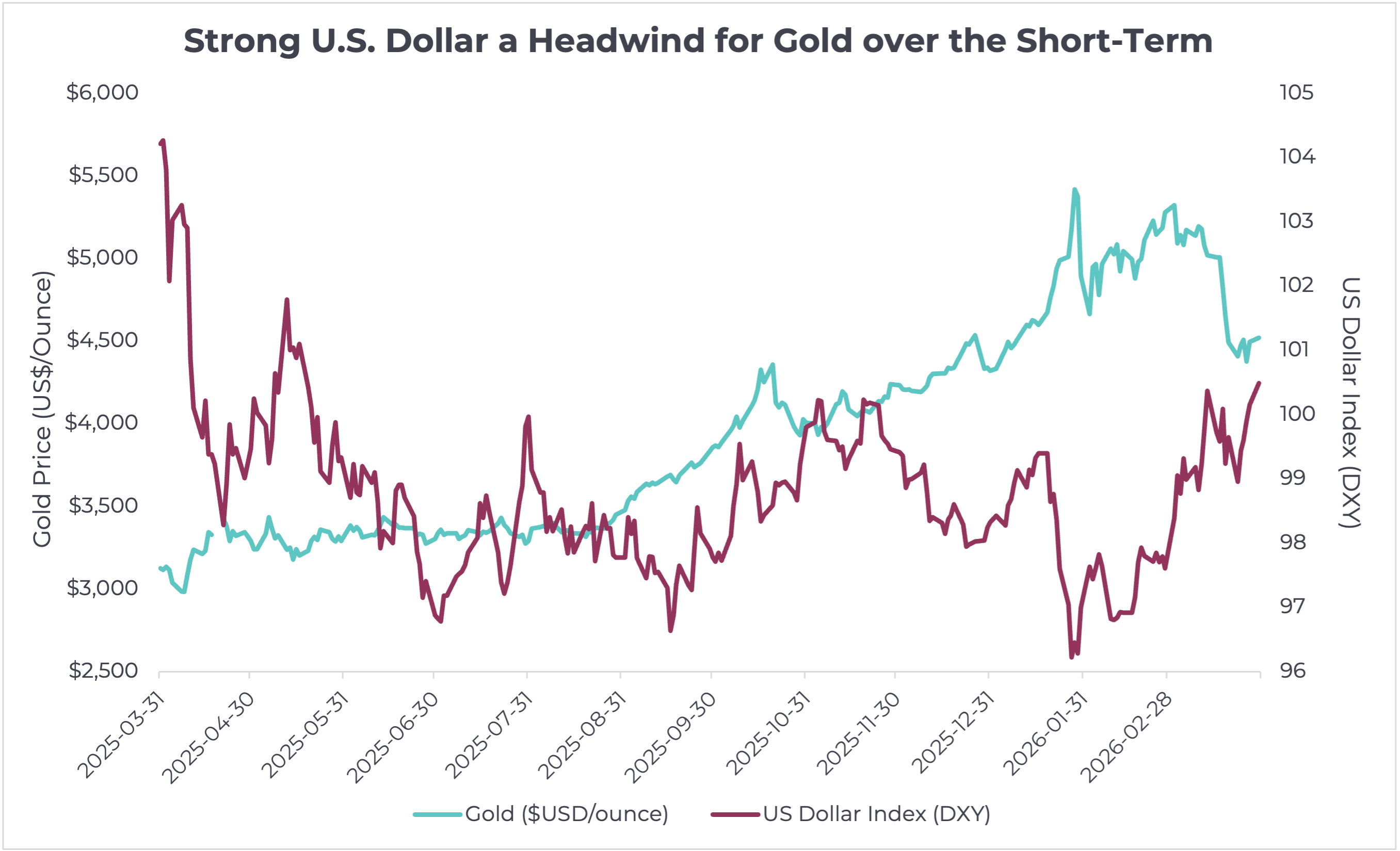

In the near term, however, gold’s behaviour can appear counterintuitive. Despite rising geopolitical tensions, gold does not always move higher, as market dynamics during periods of stress are often driven less by fundamentals and more by liquidity.

As geopolitical risks rise, oil prices tend to increase, placing pressure on growth and risk assets. As risk assets weaken, positions built on leverage begin to unwind, creating demand for liquidity — most notably in U.S. dollars. This process leads to a strengthening of the U.S. dollar, which can act as a headwind for gold in the short term, even as underlying risks remain elevated.

In this context, gold’s short-term performance is less a direct reflection of geopolitical risk, and more a function of the liquidity response that follows. Conversely, during periods of improving risk sentiment and easing financial conditions, a weaker U.S. dollar can provide support for gold alongside other assets.

In periods of stress, the system demands dollars first.

U.S. Dollar is a Headwind for Gold in Near-Term

Source: Bloomberg (as of March 30, 2026) Gold bullion vs U.S. Dollar Index

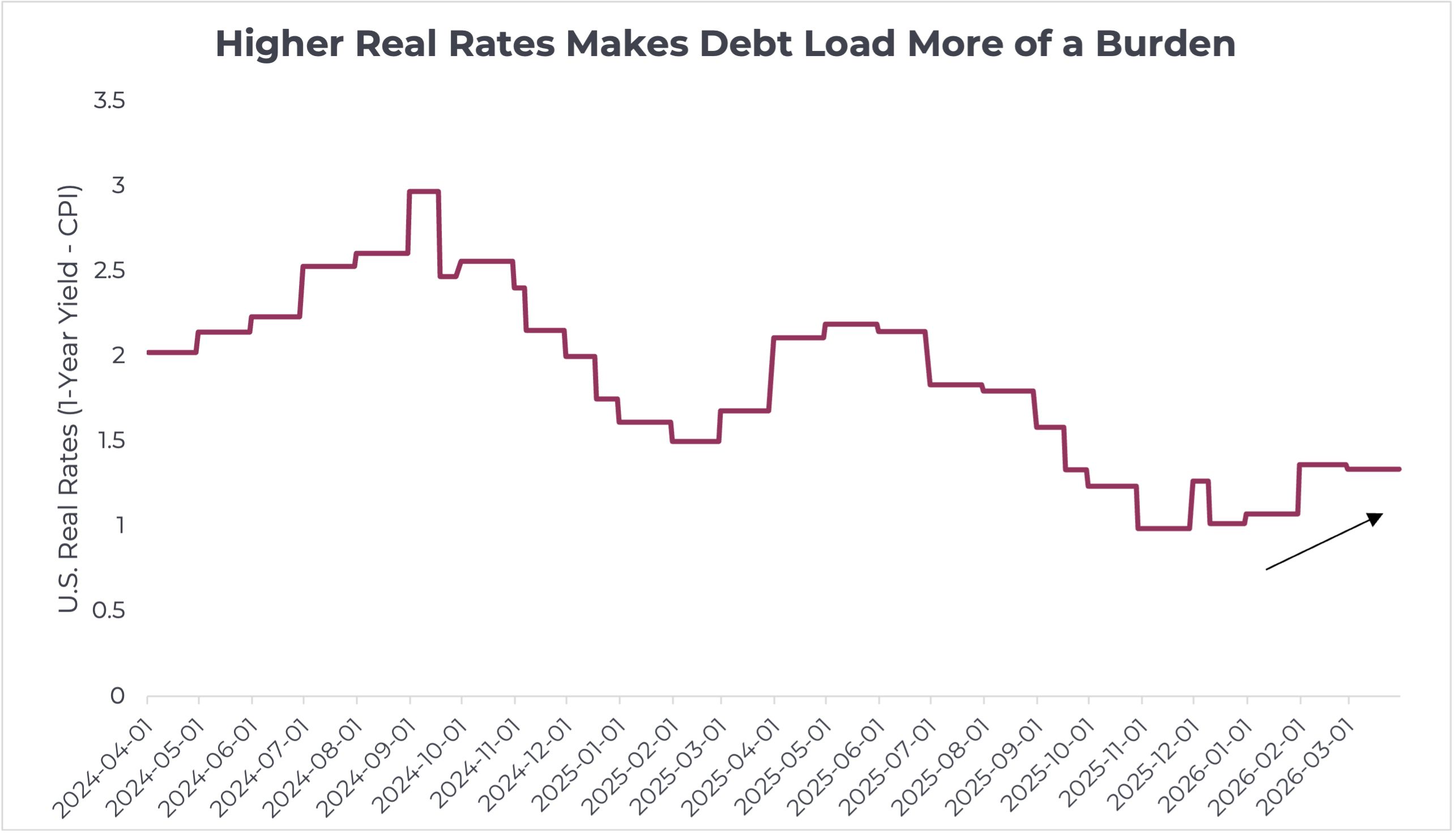

A System Under Strain: Rates and Fiscal Reality

Elevated sovereign debt levels have long implied a need for lower real interest rates over time, as financial systems rely on accommodative conditions to remain sustainable. However, recent market developments point in the opposite direction, with real rates moving higher and yields shifting upward across the curve.

At the same time, the evolving geopolitical backdrop introduces additional fiscal demands. Increased military spending and broader economic support measures add to already elevated debt levels, further expanding the supply of government issuance into a market facing higher required returns. Recent requests for additional U.S. military funding, reportedly in excess of $200 billion, highlight the scale of potential fiscal expansion and reinforce the incentive to limit the duration of the conflict.

More broadly, elevated debt levels are typically managed through a combination of growth, inflation, and financial repression, often requiring real interest rates to remain below nominal growth. A prolonged conflict complicates this dynamic, as rising energy prices push inflation expectations higher while nominal yields move up across the curve.

In practice, the increase in nominal yields has been more pronounced, resulting in higher real rates and tighter financial conditions. As both inflation expectations and nominal yields become increasingly driven by market forces, real rates become less controllable for policymakers over time, making financial repression more difficult to sustain.

This creates a fundamental tension within the system. Rising energy prices are contributing to higher inflation expectations, while tighter financial conditions are weighing on growth. In this environment, central banks face limited flexibility, easing policy risks exacerbating inflation, while maintaining restrictive conditions increases pressure on economic activity.

Source: Bloomberg (Real Rate taken as spread between 1-Year U.S. Treasury Yield and U.S. CPI – year-over year, as of March 30, 2026)

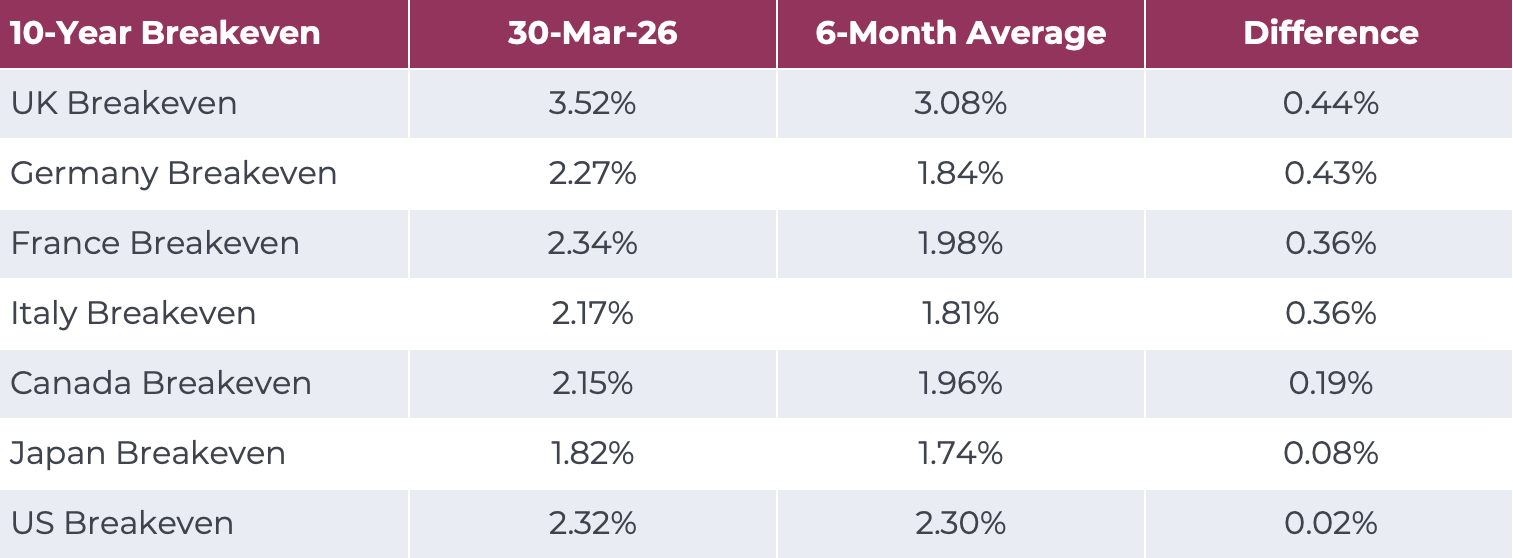

Higher Breakeven Rates mean Higher Implied Inflation

Source: Bloomberg (as of March 30, 2026 using 10-Year Breakevens)

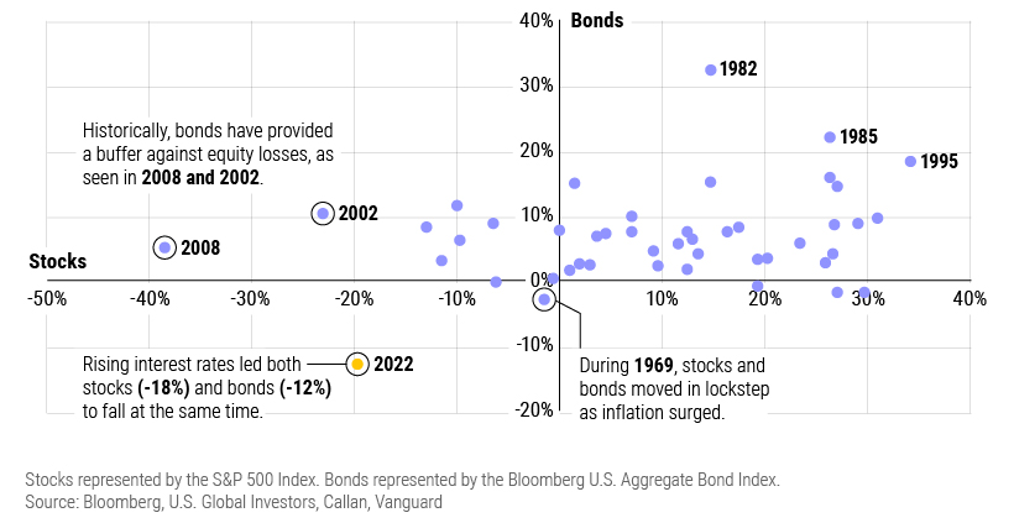

When Diversification Is Challenged

Periods such as 2022 demonstrated that traditional diversification between equities and fixed income is not constant. In environments where inflation and interest rates become the dominant drivers, both asset classes can experience negative returns simultaneously.

The current backdrop shares some similarities. Rising energy prices, higher inflation expectations, and tightening financial conditions increase the risk that both equities and bonds come under pressure at the same time, challenging the effectiveness of traditional portfolio construction.

Bonds Offer Less Protection when Inflation Risk is Present

In this context, portfolio outcomes may become more dependent on how exposures are constructed rather than broad market direction alone. While aggregate equity and bond markets may face headwinds, dispersion within asset classes tends to increase, creating a wider range of outcomes across different strategies and approaches.

At the same time, the range of potential outcomes remains wide. A de-escalation or ceasefire could lead to a rapid normalization in energy markets and a resumption of broader risk appetite, underscoring the difficulty of reacting tactically to short-term developments.

What to Watch and Staying the Course

In an environment defined by competing forces and a wide range of potential outcomes, the focus shifts from prediction to observation. Rather than attempting to forecast specific outcomes, we believe it is more effective to monitor key indicators that reflect how the system is adjusting in real time.

Key areas to watch include:

- Oil flows through the Strait of Hormuz, as a real-time measure of supply disruption

- Oil prices and spreads, reflecting the degree of stress in global energy markets

- Real rates and long-end yields, indicating the direction of financial conditions and term premium

- U.S. dollar strength, as a proxy for global liquidity and deleveraging pressures

- Equity leadership, particularly the relative performance of high beta versus defensive segments

These indicators provide a practical framework for assessing how conditions are evolving, helping investors stay focused on underlying trends rather than short-term volatility.

While the range of potential paths remains wide, periods of uncertainty can also create opportunities as markets adjust and reprice. A de-escalation or ceasefire could support a normalization in energy markets and a continuation of broader market strength, while even more challenging scenarios can lead to greater dispersion and selective opportunities across asset classes.

In this context, maintaining a disciplined and well-constructed portfolio becomes increasingly important. Portfolios designed with resilience in mind, built to navigate a range of outcomes, are well positioned to participate in opportunities while remaining insulated against downside risks. Investors should speak with their Q Wealth Portfolio Manager to ensure their portfolio is appropriately structured and aligned with their long-term objectives.

In periods of uncertainty, market outcomes are often less about forecasts and more about how the system is forced to adjust.