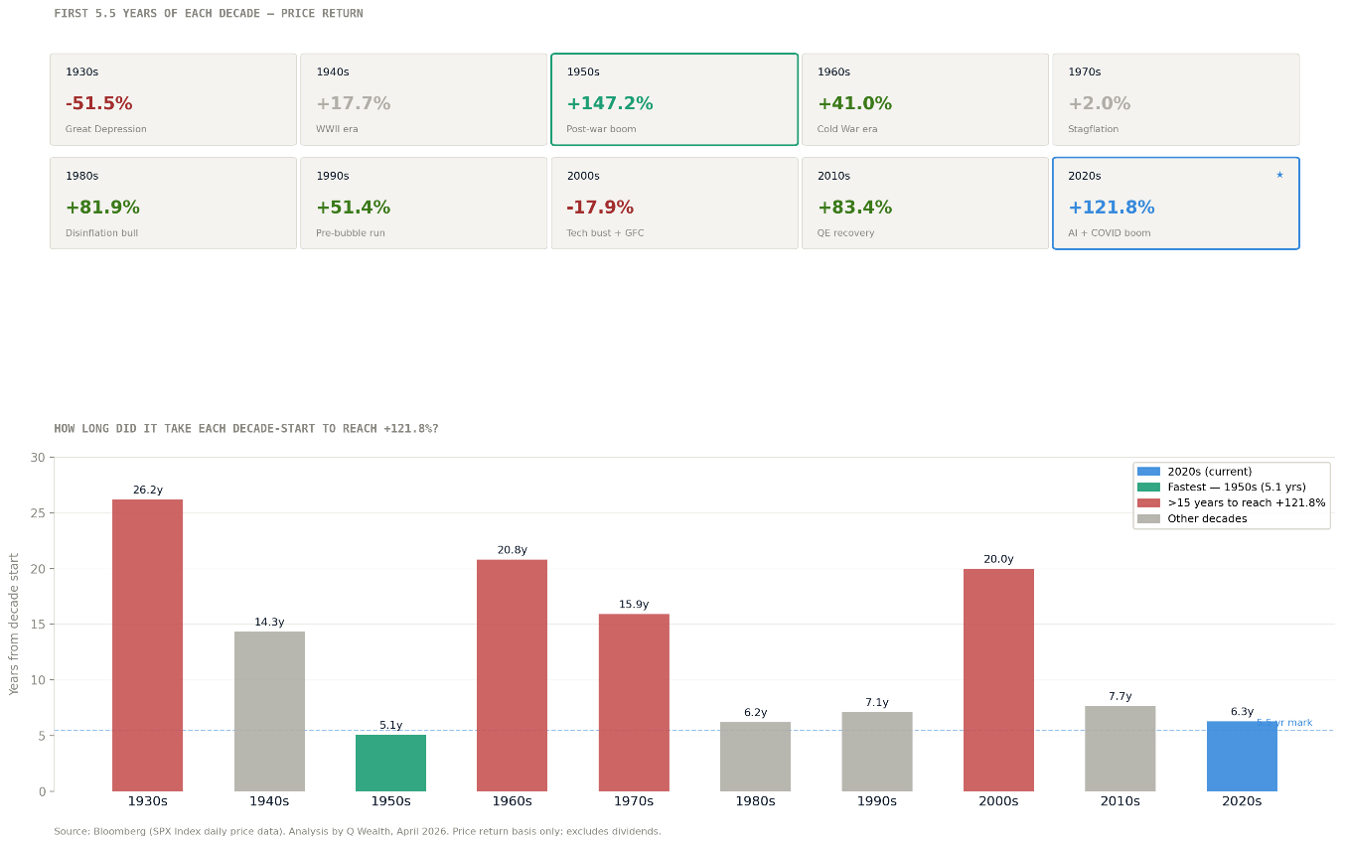

So far this decade, markets have delivered one of the strongest starts in modern history. The S&P 500 is already up roughly 120%+ in just over five years. To put that into perspective, when you compare the first half of each decade going back nearly a century, the 2020s rank among the strongest on record. Only one period clearly stands out as stronger—the post-war boom of the 1950s, which saw a +147% return over a similar timeframe.

But what’s arguably more important than the magnitude… is the speed. Historically, it has taken markets 10, 15, even 25+ years to achieve similar cumulative returns.

A Historically Extreme Run—By Any Measure

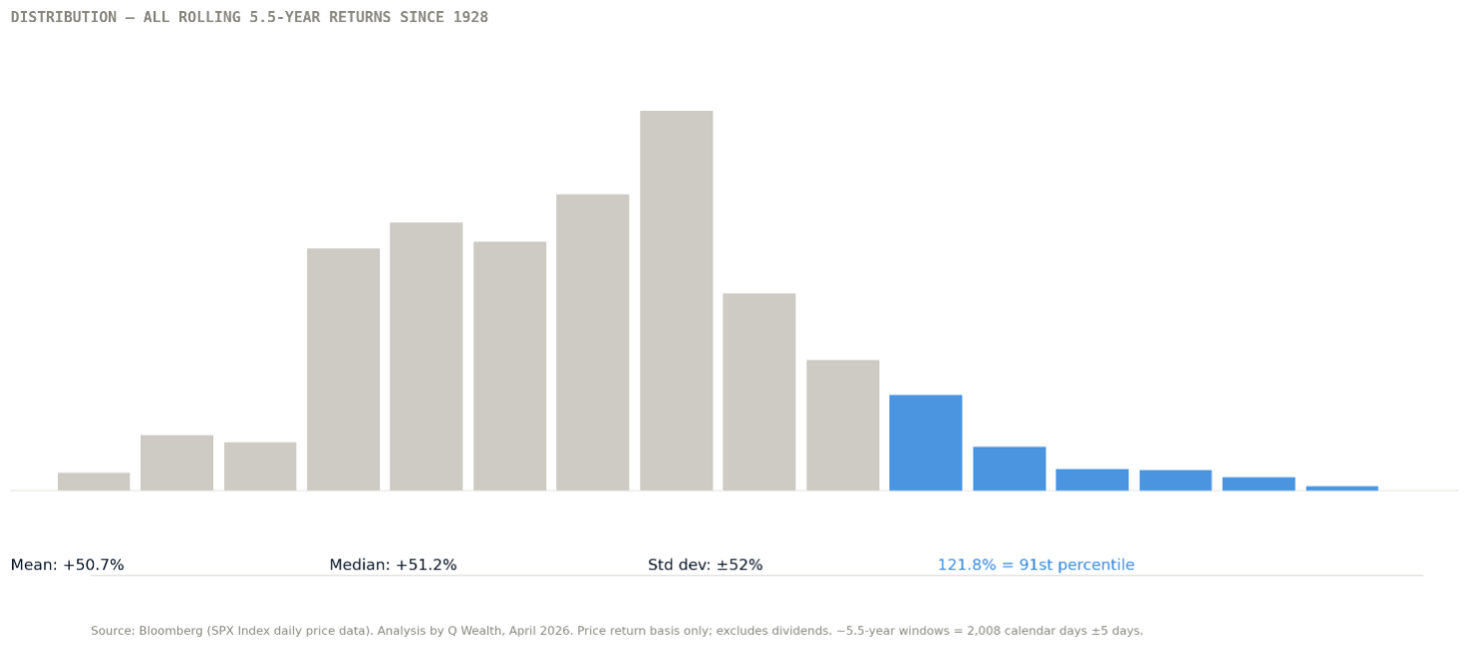

Looking beyond decades and focusing on rolling return periods gives an even clearer picture of just how unusual this cycle has been. Across all 5.5-year rolling periods since 1928, the average return for the S&P 500 has been roughly +50%, with a median just above that at +51%.

The current cycle is +121.8%. That places it in approximately the 91st percentile of all rolling periods over nearly a century.

In other words, this isn’t just a strong run—it’s statistically rare.

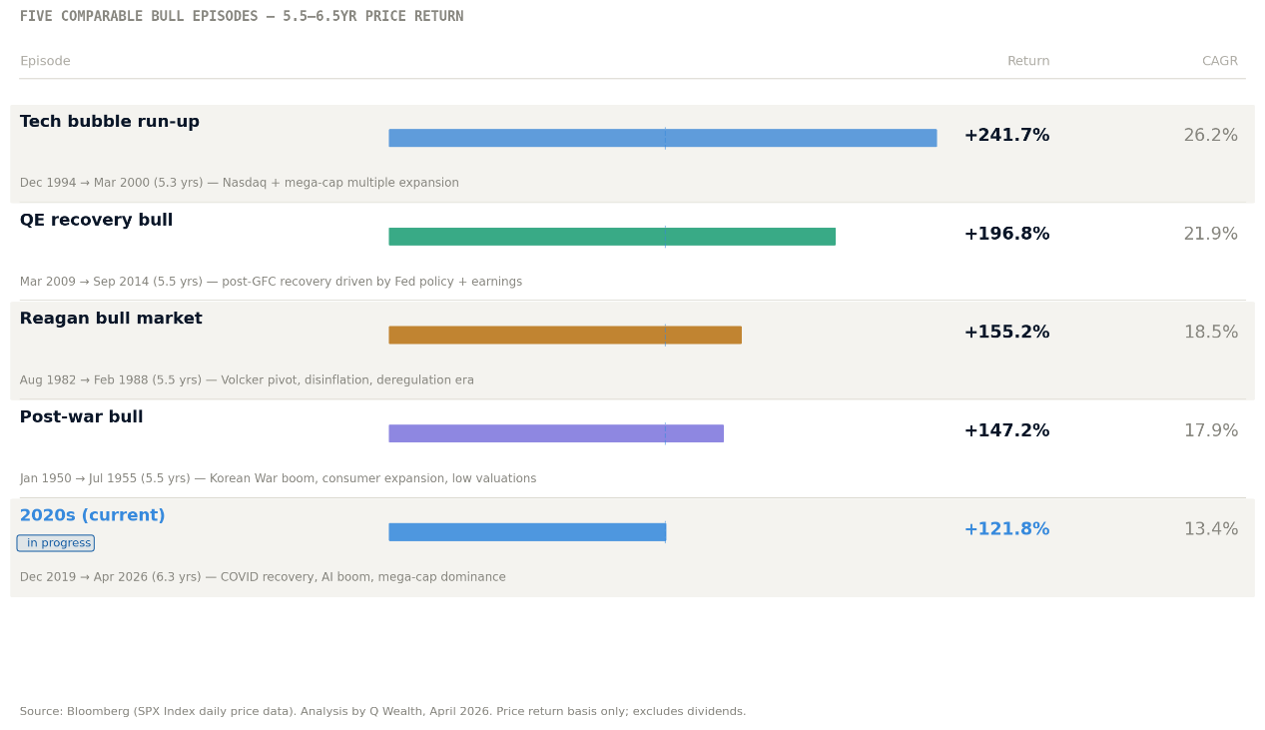

Comparable to the Most Powerful Bull Markets in History

When you stack the current cycle against historical bull markets over similar timeframes, it becomes even more clear where we sit:

- Tech bubble run-up (late 90s): +241.7%

- Post-GFC QE recovery: +196.8%

- Reagan-era bull market: +155.2%

- Post-war expansion (1950s): +147.2%

- 2020s (current): +121.8% (and still in progress)

While not the most extreme, the current run is firmly in the same tier as some of the most powerful equity expansions ever observed.

The Rise of BTFD

Bull markets don’t just generate returns—they shape investor behavior. And this one, particularly in the post-COVID period, has helped create a new type of investor. Younger. More retail-driven. Highly conditioned by one consistent outcome: “Buy the Dip.”

Often referred to as the “BTFD” crowd (Buy the “Effin” Dip), the term originated as trading slang in crypto and equity markets—an almost reflexive call to action whenever prices fall.

The underlying assumption is simple:

- Every decline is temporary.

- Every sell-off is an opportunity.

- Every dip will be followed by a recovery.

And for most of this decade… that assumption has been right. Repeatedly. Markets have consistently rebounded from 10–15% pullbacks, often with surprising speed and force. What historically might have been considered a correction has instead become a buy signal.

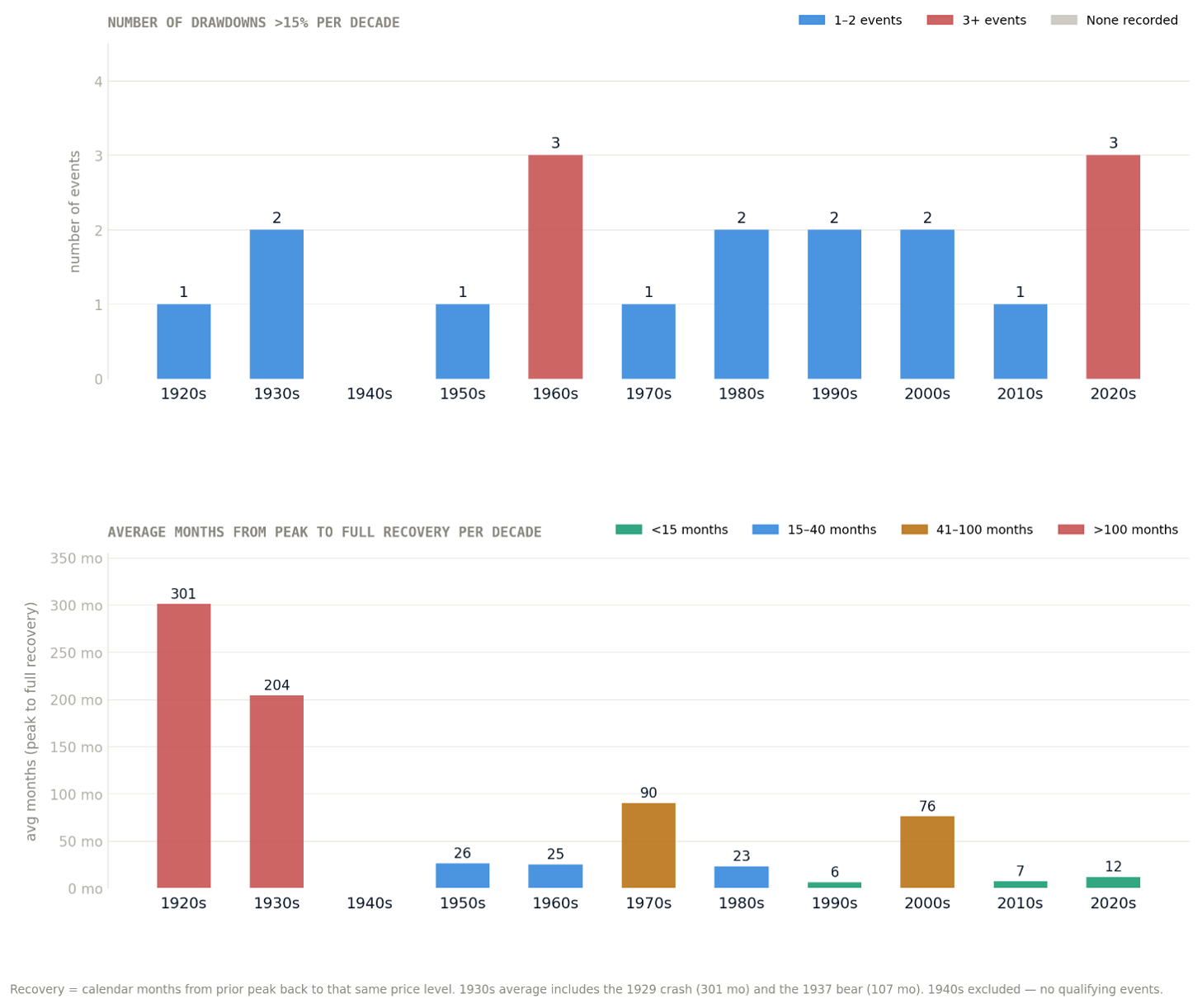

Four major sell-offs. Four very different reasons, same quick rebound

- 2020 — COVID Crash

A global economic shutdown. Entire economies brought to a standstill.

The S&P 500 fell 33.9%—the fastest drawdown in modern history. And yet, it snapped back just as quickly, fueled by unprecedented policy support.

- 2022 — The Rate Shock

After years of QE and fiscal stimulus, inflation—dormant since the 1970s—came roaring back.

Central banks responded with the most aggressive hiking cycle in four decades, alongside quantitative tightening. Liquidity was no longer abundant—it was being pulled. The S&P 500 dropped 25.4%.

- 2025 — Tariff Shock (“Liberation Day”)

A sudden shift in global trade policy, with sweeping tariffs introduced to address structural imbalances.

Markets repriced quickly, with the S&P 500 falling 18.9% as uncertainty around global growth surged.

- 2026 — Geopolitical Shock

A full-scale military conflict between the U.S., Israel, and Iran. The Strait of Hormuz closed. Global energy markets repriced overnight. And yet — the S&P 500 fell only 8.7%. This one isn't over. We don't know how it ends. But what's already remarkable is that markets, facing what would historically be considered a tail risk event, have once again found a floor — and investors have once again started buying.

What’s Really Driving the Market

The repeated, rapid recoveries this decade haven’t just rewarded investors—they’ve changed how they behave. While the number of significant drawdowns (>15%) has increased, the time required for markets to recover has been exceptionally short relative to most historical environments.

For many—particularly newer, retail-driven investors—diversification has taken a back seat. Why diversify when one strategy has consistently worked?

- Buy equities.

- Buy the dip.

- Repeat.

This “BTFD” mindset hasn’t just been reactive—it has become a source of support in the market itself.

Each pullback is met with buying.

Each sell-off finds a floor.

Equities remain well bid, even as volatility and macro uncertainty increase.

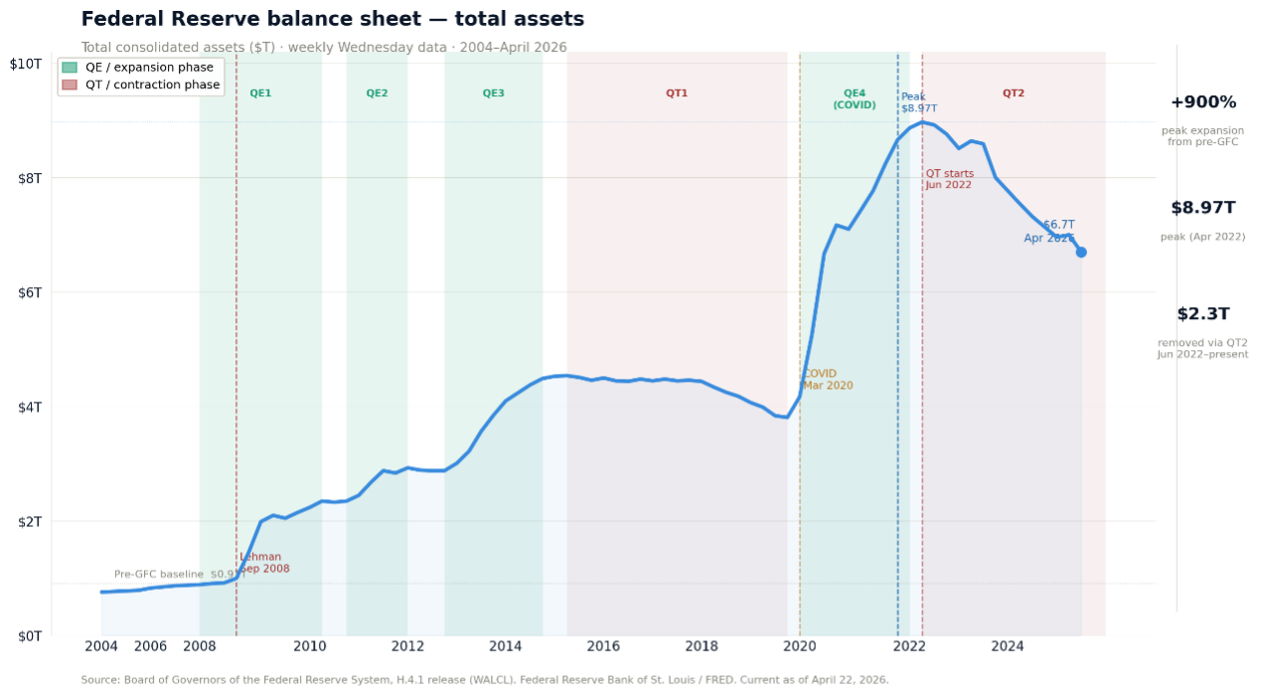

The Liquidity Engine Behind It

But behind the scenes, this resilience hasn’t been purely behavioral. It’s been structural. The post-COVID rally has been underpinned by a massive expansion in central bank balance sheets, led by the Federal Reserve. Trillions of dollars of liquidity were injected into the system—effectively increasing the amount of capital chasing a finite pool of financial assets.

At the same time:

- Interest rates remained historically low (at least initially)

- Financial conditions were highly accommodative

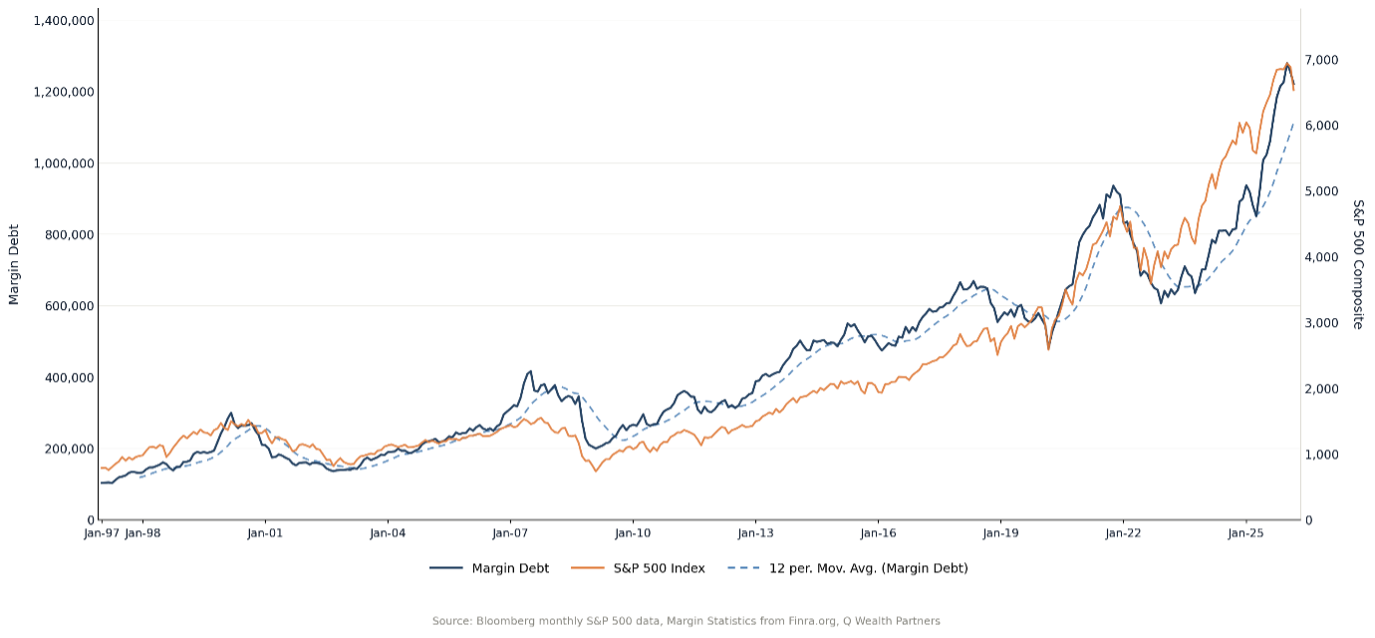

- Leverage increased, with margin debt rising alongside equity prices

The result?

A powerful feedback loop:

- Liquidity drives asset prices higher

- Rising markets encourage more participation

- Participation fuels further inflows and leverage

Which helps explain why markets have maintained such a strong underlying tone—even in the face of inflation shocks, policy tightening, and geopolitical events.

Policy Incentives Matter

This dynamic isn’t accidental.

As we’ve discussed in prior outlooks, central banks are structurally incentivized to run negative real interest rates over time—effectively allowing inflation to erode the real value of outstanding debt.

That backdrop suggests that, over the long run, liquidity is likely to remain supportive, even if it fluctuates in the short term through periods of quantitative tightening (“QT”).

Where the Risk Lies

The risk isn’t that this system suddenly disappears. It’s that it becomes constrained. At some point—whether driven by inflation, policy error, or an exogenous shock—the market could face a deleveraging event, similar to what we saw in 2008 or 2020. This isn’t meant to alarm investors—crises are a normal part of market cycles.

But when they occur, the dynamics shift quickly.

In that environment:

- Margin debt contracts

- Forced selling emerges

- Liquidity becomes less responsive

And that’s where the real vulnerability lies. The same forces that supported BTFD may not be there—especially in a stagflationary environment, where inflation effectively handcuffs central banks and constrains their ability to flood the system with liquidity.

Final Thoughts

All of this helps explain why “S&P and chill” has worked. In a market defined by rapid recoveries and structural liquidity support, discipline has often felt unnecessary—even naïve. And if your time horizon is long enough and your stomach is strong enough, maybe it still is.

But BTFD is a strategy built on one assumption: That someone will catch you if you fall.

For most of this decade, that someone has been the Fed. Rates were cut, balance sheets expanded, and liquidity flooded into the system. Every time the floor cracked, policy filled it back in. Investors learned—rationally—that falling wasn’t all that dangerous.

But inflation changes that relationship. A Fed constrained by persistent price pressures can’t respond the same way it did in 2020. And when the safety net tightens, the dynamics can shift quickly.

Margin doesn’t unwind gradually—it snaps. Leverage doesn’t fade—it collapses.

And the investors most conditioned to buy every dip can quickly become the first forced sellers. We’re not ringing alarm bells. If anything, we’ve been structural bulls throughout this cycle. But there’s a difference between being bullish and being undisciplined. One is a view. The other is a habit. And habits formed in unusually forgiving markets tend to get tested in less forgiving ones.

So yes—BTFD may still work. But it’s no longer a strategy. It’s a bet that someone catches you if you fall. And right now… that someone has their hands a little more tied than usual.