A Structural Shift in the Investment Landscape

In previous blogs and outlook reports, we have discussed the concept of a structural debasement regime — a macroeconomic environment where rising sovereign debt burdens increase the likelihood that policymakers prioritize nominal growth and financial repression over fiscal austerity. Given the number of questions we’ve received from readers and clients, this piece aims to explore that framework in greater detail — examining not only the forces driving this shift, but also what it may mean for portfolio construction in the years ahead.

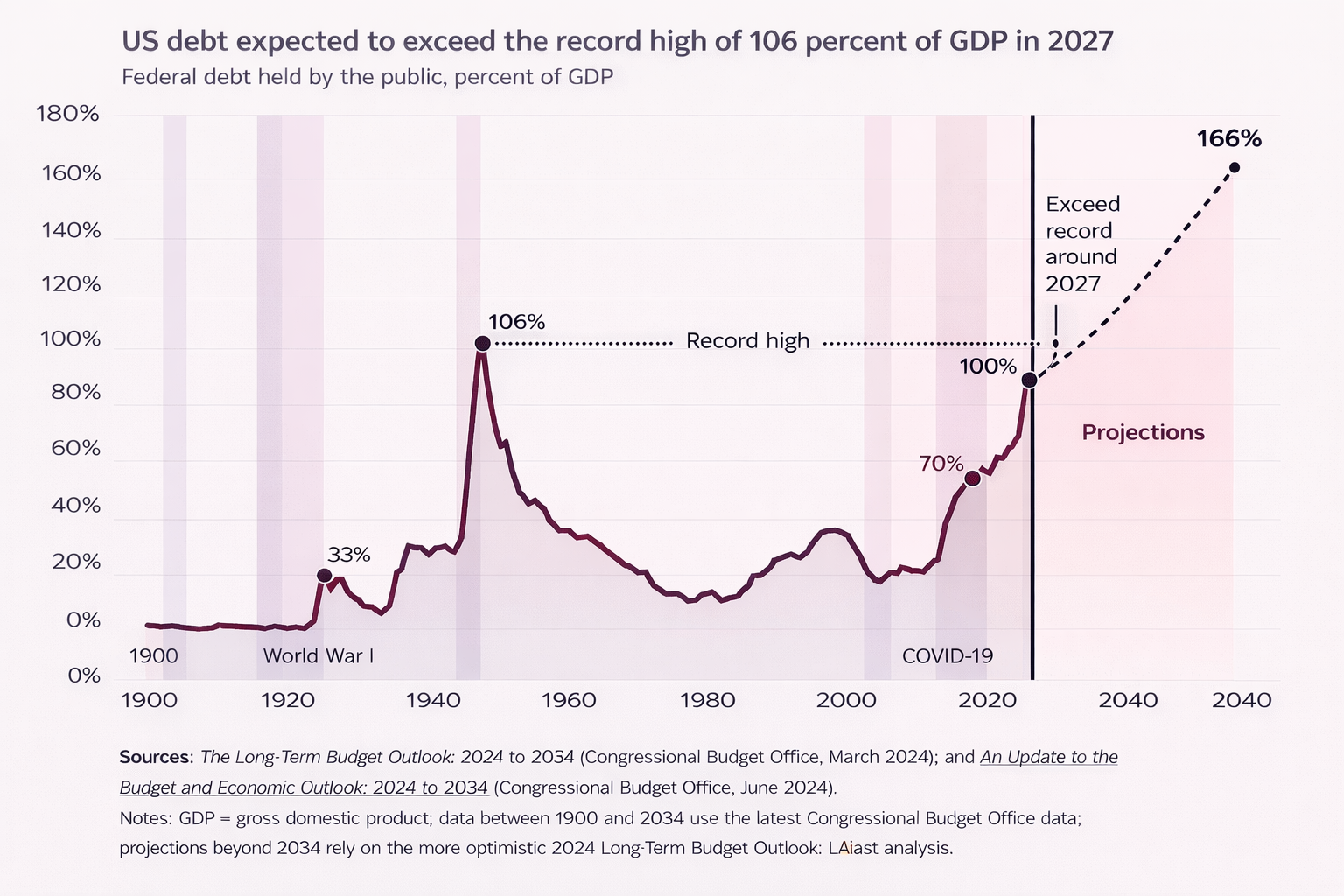

While much of the discussion has centered on the United States, this is not a single-country phenomenon. Debt-to-GDP levels are rising across both developed and emerging markets, accelerated by the Global Financial Crisis, pandemic-era stimulus, and a growing reliance on unconventional monetary policy tools.

Central banks around the world have expanded their playbooks beyond traditional rate cycles, normalizing measures such as quantitative easing, forward guidance, and targeted liquidity support. As these policies become embedded within the global financial system, investors must increasingly consider how persistent debt expansion influences long-term asset returns.

The question facing markets today is not whether debt levels are high — but how governments choose to manage them.

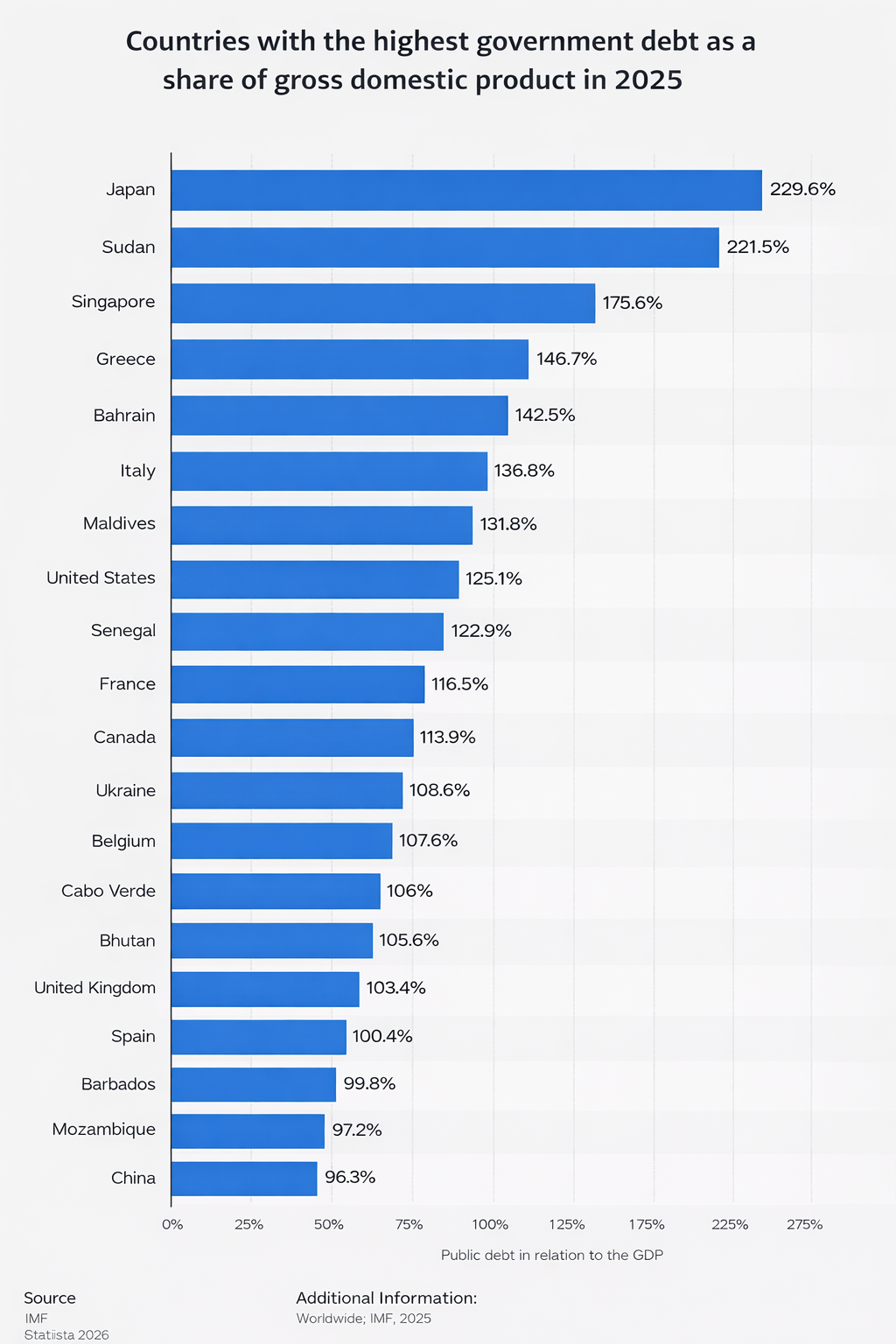

Countries With the Highest Government Debt/GDP

Source: Statista, IMF, 2025

How Countries Historically Reduce Debt Burdens

History suggests that sovereign debt ratios decline through only a handful of mechanisms:

1) Fiscal Austerity

Governments can attempt to reduce deficits through spending cuts or higher taxation. In practice, sustained austerity has proven politically difficult, particularly in democratic systems where short-term economic contraction often conflicts with electoral incentives.

2) Default or Restructuring

Outright default remains highly unlikely for large developed economies, particularly the U.S. which is looking to maintain its reserve-currency status. Preserving confidence in sovereign debt markets remains a core policy priority.

3) Growing Out of Debt

Strong economic growth can lower debt ratios organically. However, aging demographics across much of the developed world present structural headwinds to labor-force expansion.

Technological innovation — particularly artificial intelligence — may partially offset these pressures by amplifying productivity and enabling workers to scale output more efficiently. At the same time, technological disruption introduces transitional challenges, including workforce displacement and uneven income dynamics.

4) Inflation and Financial Repression

Historically, many highly indebted economies have relied on a combination of modest inflation and suppressed real interest rates. When nominal yields remain below inflation for extended periods, debt burdens gradually decline in real terms — a process often described as financial repression.

Rather than relying on a single solution, policymakers often pursue a blend of growth and inflation, allowing debt levels to stabilize without abrupt fiscal tightening.

A Global Phenomenon — Not Just a U.S. Story

Although U.S. debt levels receive significant attention, the broader trend is global. Governments across regions are expanding fiscal commitments in response to:

- Aging populations and rising social expenditures

- Strategic investment in artificial intelligence (AI) and technological leadership

- Increasing geopolitical fragmentation and higher defense spending

- The normalization of unconventional monetary policies

As global economies become increasingly fragmented, policy responses are still evolving along similar lines. Despite reduced globalization and rising geopolitical divisions, many nations face comparable fiscal pressures, creating a shared macro backdrop — one where currency dilution and suppressed real yields may become structural features rather than temporary anomalies.

For investors, this represents a regime shift rather than a cyclical event.

The Historical Playbook: Negative Real Rates Are Not New

Periods of elevated debt have frequently coincided with environments where real interest rates remained low or negative:

- World War II Era: Nominal yields were held low while inflation rose, reducing debt burdens over time.

- 1970s Inflationary Period: Inflation consistently exceeded nominal rates, compressing real returns on fixed income.

- Post-Dotcom Recovery: Aggressive easing resulted in extended periods of low real rates.

- Global Financial Crisis: Zero-rate policy and quantitative easing drove prolonged negative real yields.

- Pandemic Response: Near-zero rates combined with elevated inflation once again pushed real yields below zero.

These episodes illustrate that financial repression has often emerged as a policy response in high-debt environments — even if it comes at the expense of savers and long-term purchasing power.

Implications for Investors: Alpha Is Evolving

If the coming cycle is characterized by persistent debt expansion and structurally lower real yields, traditional sources of outperformance may continue to evolve.

In prior decades, investors often relied on market timing and/or individual security selection to generate alpha. Today, the opportunity set is shifting.

Alpha is increasingly driven by:

- Portfolio construction and structural diversification

- Factor exposures aligned with macro regimes

- Tax-aware implementation and long-term compounding

The foundations of portfolio construction are shifting. Historical allocations that performed well during disinflationary cycles may require reassessment as macro regimes evolve. Fixed income remains an essential component of diversification and downside protection, yet an overreliance on conventional equity–bond structures may expose portfolios to prolonged periods of negative real yields.

Complementary exposures to traditional portfolios may include:

- Real assets such as infrastructure, land, and commodities

- Precious metals, including gold and silver

- Private market investments across equity, credit, and real assets

- Alternative strategies designed to navigate inflationary and regime-shift environments

The objective is not to replace core allocations, but to enhance portfolio resilience — broadening the opportunity set while helping portfolios adapt to evolving macroeconomic conditions.

The Emerging K-Shaped Economy

A prolonged period of financial repression may also reinforce a widening gap between asset owners and those who remain uninvested. Historically, environments characterized by rising asset prices alongside suppressed real yields have contributed to increasing social pressures and calls for expanded fiscal support — dynamics that can further reinforce debt expansion.

For investors, this underscores the importance of participation. Remaining on the sidelines carries its own long-term risk: the gradual erosion of purchasing power.

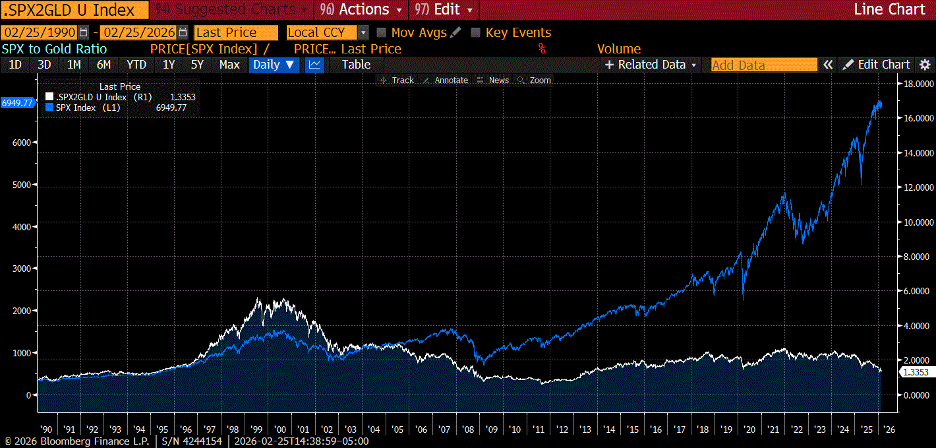

One way to illustrate this dynamic is through the lens of real assets. While the S&P 500 Composite has experienced a significant nominal rise in the post-Global Financial Crisis era, a different perspective emerges when equities are measured against hard assets such as gold. When priced in gold — a proxy for real purchasing power — equity markets have remained relatively flat over extended periods.

This does not suggest that equities have failed to generate value. Rather, it highlights that a meaningful portion of nominal asset appreciation may reflect the declining purchasing power of fiat currencies, not solely organic economic growth. Nominal returns can appear strong even as the measuring stick itself is being diluted.

In a debasement regime, investors are not simply seeking returns — they are seeking to preserve and grow real wealth, adjusted for inflation. Owning productive assets such as equities, real assets, and alternative strategies becomes increasingly important, not as a tactical decision, but as a structural response to an evolving macroeconomic environment.

This does not mean abandoning fixed income. Cyclical dislocations — at times, may even be comparable to 2008 or 2020 — reinforce the need for duration exposure to help offset equity risk during periods of stress. Yet over the long term, equities and real assets have historically been the primary drivers of real wealth creation for asset owners.’

S&P 500 Has Gained but Remained Flat Priced in Gold

Source: Bloomberg (February 25, 1990 to February 25, 2026)

The Importance of Staying Invested

In a world where negative real rates quietly reshape financial outcomes, the greatest challenge may not be volatility — but inactivity.

Holding excess cash or relying heavily on short-term instruments may feel defensive, yet over time, suppressed real yields can diminish long-term wealth accumulation.

Rather than attempting to time policy shifts or predict macro turning points, investors may benefit from focusing on what remains within their control:

- Maintaining disciplined exposure to productive assets

- Constructing portfolios designed to endure multiple economic regimes

- Optimizing tax efficiency to enhance compounding over time

The next decade may not reward the smartest stock pickers as much as it rewards the most structurally prepared portfolios.

In a global debasement regime, success will likely come not from predicting the future — but from building portfolios resilient enough to navigate it.

Disclosure:

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.