Market Recap: Q3 2025 Performance

Global markets extended their gains in the third quarter, buoyed by a combination of dovish policy expectations, resilient economic data, and strong corporate earnings. Equity markets posted robust advances, with the S&P 500 Composite rising 8.11%, the S&P/TSX Composite gaining 12.50%, and the MSCI EAFE up 4.87% (in USD terms), reflecting broad-based risk appetite. Commodities also strengthened, led by a 16.83% surge in spot gold and a 6.27% advance in Bitcoin — increasingly viewed as a digital counterpart to bullion — as investors sought hedges against higher inflation expectations and mounting concerns over government debt sustainability. Meanwhile, fixed income delivered more modest returns, with Canadian bonds up 1.49% amid shifting interest rate expectations (all returns in local terms unless otherwise noted).

In addition, markets have been undergoing a period of normalization following the sharp Liberation Day sell-off in April. Over the past quarter, several countries have reached tariff agreements with the U.S., easing one of the more prominent geopolitical headwinds. While investors are still awaiting the Supreme Court’s ruling on the constitutionality of these tariffs, the issue has largely faded from the headlines for now. Within this backdrop, we have remained constructive on risk assets, recognizing the resilience of earnings and the broader U.S. economy. However, with equity markets having rallied sharply this year and much of the market’s strength concentrated in AI-driven capital expenditure themes, investors may want to exercise greater selectivity and consider protecting some of those gains. As we head into the final quarter of 2025, we believe the focus will center on four key themes: interest rates, valuations, consumer and credit health, and the geopolitical landscape. And just like in sports, with the S&P 500 Composite up 14.8% and the TSX up 23.9% year-to-date, the fourth quarter is about defending the lead — ensuring that strong gains are sustained, not surrendered, as the year closes out.

Risk Assets Continue to Move Higher

Source: Bloomberg, Q3 2025 are total returns between 06/30/2025 and 09/30/2025, YTD returns are between 12/31/2024 and 09/30/2025. All returns are expressed in USD except for S&P/TSX Composite and Canadian Bonds which are expressed in CAD.

Interest Rates: From Hawkish Resolve to Risk Management Cuts

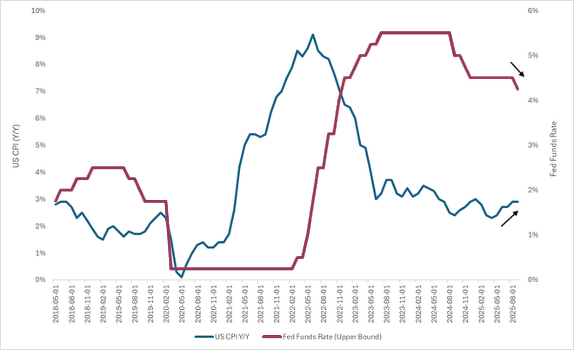

Earlier this year, Fed Chair Jerome Powell struck a distinctly hawkish tone, stressing that more clarity on tariffs was needed before considering any rate cuts. While the labor market has shown some signs of weakening, the broader U.S. economy remains relatively robust. Under increasing pressure from the Trump administration to ease policy, Powell has now delivered what he described as a “risk management” cut — intended as insurance in case the economy slows abruptly.

This move, however, appears inconsistent with his earlier position that the Fed cannot simultaneously stimulate the economy and fight inflation. The decision to cut while inflation is re-accelerating raises questions around policy credibility. U.S. year-over-year CPI has moved higher from 2.7% to 2.9%, brushing the upper end of the Fed’s target range, while the Fed’s preferred measure, core PCE, has also edged higher. Compounding the uncertainty, Powell refrained from offering clear forward guidance on the path ahead, while notably doing little to push back against market expectations for two additional cuts by year-end.

Markets remain divided on whether this cut was warranted. Our focus looking forward is twofold: first, whether additional easing inadvertently fuels inflationary pressures, which could ultimately force the Fed back into tightening at some point further down the road — a scenario that would be a headwind for the current bull market as markets are forward looking; and second, whether confidence in Fed independence erodes, potentially driving long-term rates higher over time.

For a more detailed discussion of both Fed and Bank of Canada policy shifts, see our recent blog post: “Tale of Two Rate Cuts.”

Easing into an Inflation

Source: Bloomberg

Valuations: Looking Under the Hood

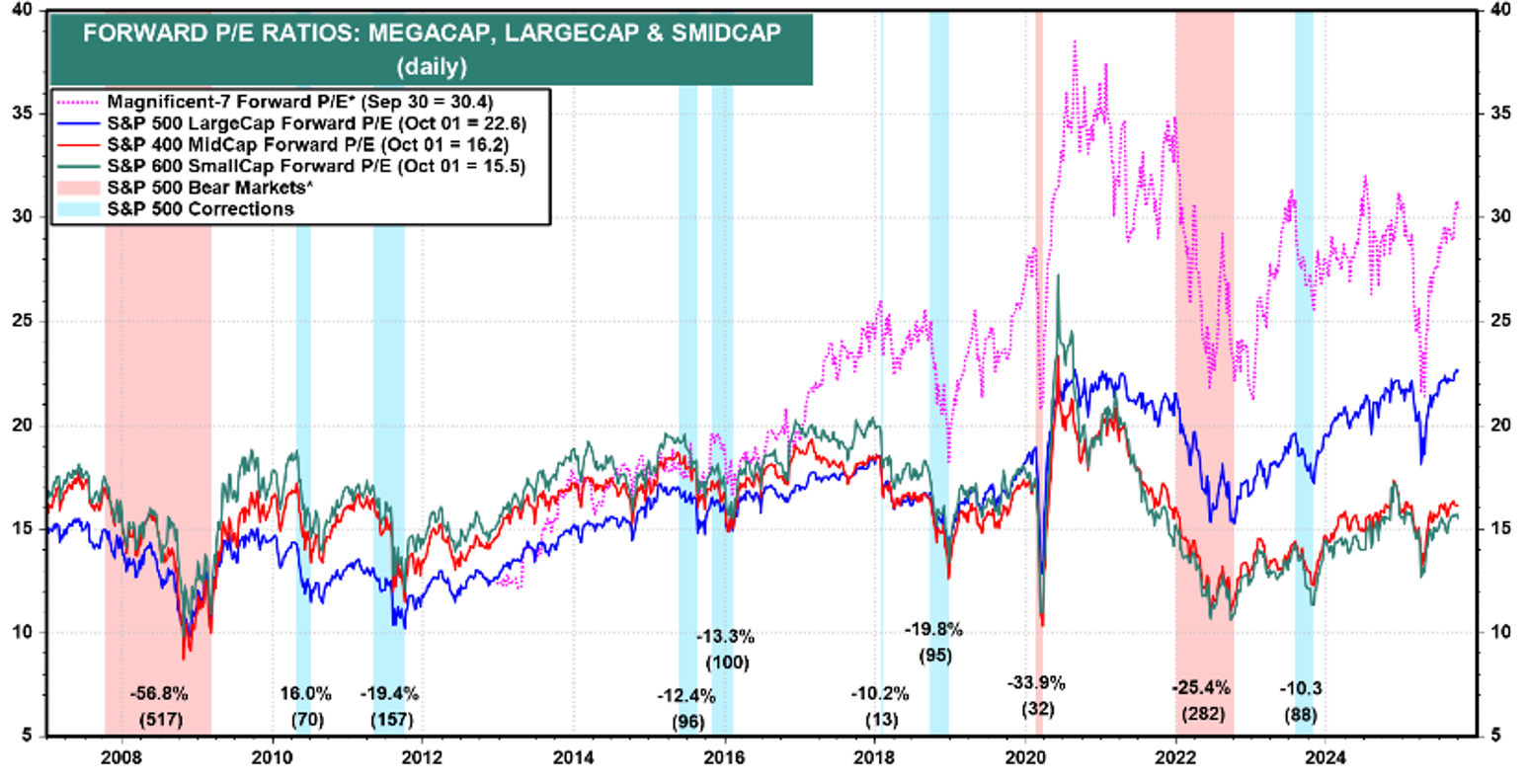

Concerns over market valuations have been a recurring theme, with headline measures such as the S&P 500 forward P/E suggesting that equities are trading above historical averages. While this surface-level view points to stretched valuations, much of the “froth” is concentrated in the Magnificent Seven stocks, which continue to command premium multiples. Outside of this narrow cohort, the broader market — particularly mid- and small-cap equities — appears far more reasonably priced.

Another important nuance is the role of earnings expectations. Analysts often set forecasts conservatively, guided by corporate management teams, which has contributed to the high percentage of earnings beats in recent quarters. In fact, 83% of S&P 500 companies exceeded earnings estimates last quarter, with average profit margins coming in 8.3% above forecasts. This suggests that headline multiples may overstate how expensive equities truly are. When adjusted for growth — as measured by the PEG ratio (Price-to-Earnings divided by expected earnings growth) — valuations look far less demanding, indicating that current price levels are not inconsistent with earnings momentum and margin resilience.

Finally, the valuation gap between large caps and their mid- and small-cap counterparts remains historically wide. For clarity, we often refer to this group as SMID caps (Small- and Mid-cap companies). Should the rate-cutting cycle progress and economic conditions remain supportive, lower interest rates could provide a meaningful tailwind for SMID-cap equities, which have lagged significantly. Taken together, these factors reinforce our view that valuations must be decomposed and contextualized rather than judged solely on headline multiples. Beneath the surface, the opportunity set appears more balanced — another reason we remain constructive, though we believe a short-term consolidation is not only needed, but healthy as it would allow for corporate earnings to catch up with prices.

Source: LSEG Datastream and Yardeni Research.

*Corrections are declines of 10% or more (blue shades). Bear markets are declines of 20% or more (red shades). Number of days in parentheses.

Source: LSEG Datastream and Yardeni Research.

*Forward P/E divided by LTEG, which is 5-year forward consensus expected annual earnings growth. Monthly through 2025, then weekly.

**Corrections are declines of 10% or more (blue shades). Bear markets are declines of 20% or more (red shades). Number of days in parentheses.

The Real Economy: Labor Market in Transition

The labor market has increasingly become the focal point for assessing the health of the real economy. Recent data shows a clear cooling trend: payroll growth has slowed with prior months revised lower, the unemployment rate has risen to 4.3% (August 2025), and the average workweek has declined to 34.2 hours as employers trim hours before reducing headcount. At the same time, average hourly earnings rose 0.3% in August, but real earnings slipped 0.1%, reflecting the drag from inflation on household purchasing power.

This has fueled the debate over whether the slowdown in employment is primarily a supply-side or a demand-side issue. On the supply side, tighter immigration enforcement and policies from ICE have reduced labor availability, creating structural shortages in certain sectors. If supply remains the binding constraint, lower interest rates will do little to ease labor market tightness and may only add fuel to inflation. On the demand side, however, the evidence is mounting that employers are pulling back due to softer revenue growth and rising costs: slower job creation, higher unemployment, and moderating wage growth all suggest weakening labor demand rather than persistent shortages.

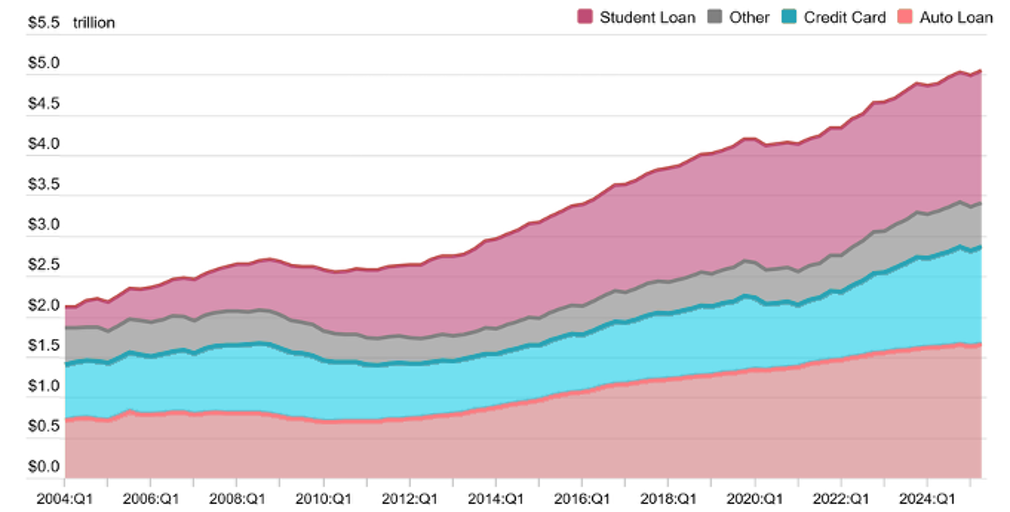

Credit conditions are adding another layer of pressure. Household savings built up during the pandemic have largely been depleted, while credit card delinquencies have been edging higher. Banks have also reported tighter lending standards, making it more difficult for households and smaller businesses to access credit. For lower-income households in particular, the combination of softening real wages and reduced credit availability is beginning to constrain discretionary spending.

The key concern is whether this evolving backdrop limits consumer spending, which in turn would mean slower revenue and earnings growth for companies. At this stage, we do not view this as an immediate risk, but it is a trend we are closely monitoring. Even if some deterioration in labor conditions is necessary to relieve inflationary pressures, the balance between cooling inflation and preserving consumer resilience will remain a defining factor for markets heading into 2026.

Non-Housing Debt Balance

Source: FRBNY Consumer Credit Panel/Equifax

Geopolitical Risks: A Source of Potential Volatility

While markets have been dominated by monetary policy and earnings, geopolitics remains an important undercurrent that could reintroduce volatility. Trade tensions have eased somewhat as a number of countries struck tariff agreements with the U.S. during the quarter. However, uncertainty lingers as the Supreme Court weighs the constitutionality of tariffs. Importantly, the Trump administration has vowed to maintain tariffs regardless of the Court’s ruling, which could translate to ongoing uncertainty for global trade and supply chains. With the 2026 mid-term elections approaching, the administration will also be eager to secure policy “wins” to maintain and expand its congressional presence — adding another layer of political complexity to market dynamics.

Beyond trade, global flashpoints continue to simmer. The war in Ukraine shows little sign of resolution, while tensions in the Taiwan Strait remain a key risk for supply chains and technology markets. In the Middle East, President Trump has introduced a 20-point peace plan for Gaza, which could either pave the way for stability if accepted, or inflame tensions further if rejected. Either outcome has the potential to affect regional security and global energy markets.

Geopolitics may not be the primary driver of returns at this stage, but they represent key sources of potential volatility that can escalate quickly. The combination of unresolved global conflicts, domestic political maneuvering ahead of the mid-terms, and persistent tariff uncertainty underscores the need for vigilance.

Positioning & Takeaways

As we head into the final quarter of 2025, markets continue to balance the tailwinds of a resilient economy and easier monetary policy with the headwinds of inflationary risk, labor market cooling, and geopolitical uncertainty. Our review of the four key themes — interest rates, valuations, the real economy, and geopolitics — suggests that while conditions remain supportive, risks are mounting beneath the surface.

On interest rates, the Fed’s recent shift toward easing may provide near-term support, but cutting into a backdrop of rising inflation raises the probability of stagflation and increases the risk of a policy misstep. On valuations, headline multiples appear stretched, yet much of the “froth” is concentrated in the Magnificent Seven, while the broader market — particularly SMID caps — remains more reasonably priced. In the real economy, the labor market is cooling and credit conditions are tightening, raising questions about future consumer resilience. Geopolitically, risks are not the primary driver of returns today, but they represent potential catalysts for volatility that can escalate quickly.

Taken together, these dynamics leave us constructive but measured in our outlook. History shows that back-to-back-to-back years of outsized equity returns rarely end well — and with sizable gains already recorded not only in equity markets but also across other risk assets year-to-date, the task now is less about chasing further upside and more about sustaining it. Put simply, the fourth quarter is about defending the lead — ensuring that the bull market continues on a more durable footing.

At the same time, markets are becoming increasingly complex, shaped by overlapping policy, economic, and geopolitical forces. This environment calls for a more strategic approach to portfolio construction. Speak to your Q-Wealth advisor today to ensure your portfolio is positioned to navigate both the risks and opportunities ahead.

Disclaimer

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.

© Quintessence Wealth. All rights reserved.