I’ve never believed in market timing. As we discussed in last week’s blog, the data consistently shows that staying invested remains the best course of action for long-term investors. The key is having a well-constructed portfolio—one that’s thoughtfully diversified across not just asset classes but also across market factors—to ensure greater stability through different environments.

That said, with so many markets—from equities and gold to digital assets—pushing to new all-time highs, a pullback (or at least a healthy consolidation) feels not only possible but necessary for earnings to catch up with price expectations.

Structurally, I continue to believe we’re in a debasement regime—a period defined by persistent fiscal deficits, mounting government debt, and ongoing policy stimulus. Unchecked government spending and the widening gap between expenditures and revenues reinforce this dynamic. With the U.S. committed to maintaining its role as the world’s reserve currency, gradual currency debasement remains the most probable long-term outcome. In that environment, real and productive assets—stocks, gold, digital assets, and other hard assets—should continue to benefit over the secular horizon.

Cyclically Speaking

I’ve been bullish for years and continue to believe the debasement regime favours equities and real assets over the long run. Structurally, that hasn’t changed. Cyclically, however, there are emerging signs of strain—a development that may actually be healthy if it leads to a modest retracement this quarter, rather than a market correction.

The Magnificent 7 continue to dominate market performance, representing an outsized share of the S&P 500’s total market capitalization and lifting aggregate valuations well above historical averages. Excluding these mega-cap names, the S&P 500 trades at a forward P/E of roughly 19.3x, only slightly above its long-term mean. Include them, and that multiple jumps to 33.1x.

That level of concentration, coupled with growing concern about the group’s circular capex spending—where companies are increasingly investing in each other’s platforms and infrastructure—introduces fragility into what has otherwise been a remarkably resilient market narrative.

Meanwhile, renewed stress in the regional banking space adds another layer of cyclicality risk. Having managed a large U.S. banking ETF through the regional banking crisis of 2022 and having researched option ARM dealers during the 2008 period, one thing becomes clear: credit concerns in that space are rarely idiosyncratic. That said, today we have far more tools to combat a potential banking crisis—such as relaunching the Bank Term Funding Program (BTFP)—which effectively expands the Fed’s balance sheet. While such measures can stabilize markets in the short term, they are inherently inflationary, which only complicates the long-term policy trade-off… but that’s a discussion for another day.

A Closer Look at Market Valuations

.png)

Low Volatility Strategies: The Brakes That Keep You Moving

Periods of market turbulence are inevitable. For investors who prefer to stay invested rather than attempt market timing, low volatility strategies provide an effective way to manage downside risk while maintaining exposure to long-term growth. They act as a stabilizer — a built-in form of risk management that helps smooth returns and keep portfolios on course, even when markets become unpredictable.

Think of them as the brakes on a car. You don’t add brakes just to slow yourself down — you add them to stay in control. They allow investors to keep participating in markets while maintaining composure through sharp turns and uneven roads.

Among the various approaches to managing portfolio risk, low volatility strategies stand out for their simplicity and effectiveness. They allocate to stocks that historically exhibit lower price variability than the market, reducing drawdowns and portfolio-level swings. Unlike minimum variance strategies, which often impose sector-neutral constraints to maintain index-like characteristics, low volatility strategies allow for more true factor exposure — capturing the behavioral and structural advantages of the low-volatility effect more directly.

For that reason, we view low volatility strategies as a better complement to the higher-growth areas of a portfolio. They’re not intended to replace growth exposures, but to enhance durability — helping investors stay invested and participate in the upside while cushioning against the inevitable pullbacks. In an environment defined by elevated valuations, persistent debt, and policy-driven volatility, maintaining that balance between participation and protection is more important than ever.

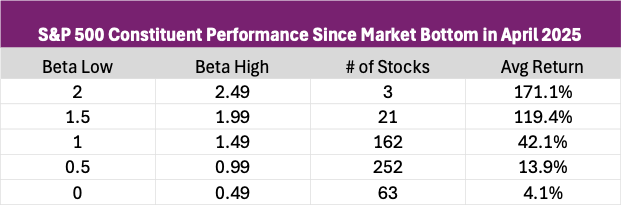

It’s worth noting that while markets have rallied since the April Liberation Day lows earlier this year, the recovery has been uneven. Much of the upside has been driven by higher-beta names, while many lower-beta counterparts have remained largely flat, contributing little to the advance. As Jamie Dimon, CEO of JPMorgan Chase, recently remarked, “when you see one cockroach, there are usually more,” suggesting that concerns in the regional banking space are rarely isolated. Against that backdrop, we could see a mean reversion trade begin to unfold, with investors rotating toward lower-beta stocks as they seek shelter from potential turbulence. Even in the absence of a market sell-off, momentum in high beta stocks can’t continue forever.

Market Rally Since the April Lows based on Beta Profile

Staying Invested Through the Noise

We continue to believe we’re in a debasement regime—a period where persistent deficits and policy intervention support the long-term appreciation of real and productive assets. While that structural backdrop favors staying invested, the path forward will remain uneven.

Low-volatility strategies help investors navigate that noise—keeping portfolios balanced, disciplined, and fully invested when markets turn choppy. In an era defined by elevated valuations and policy-driven swings, the ability to participate while maintaining composure is what separates strategy from speculation.

And with that, I’ll leave you with this fitting Matrix-inspired meme: the Merovingian, the “Trafficker of Information,” looking to disrupt the Oracle (the bull market), while Neo— Low Volatility Strategies—calmly counters within the Matrix. 😎😉

Low Volatility: Countering the “Merovingian”

Disclosure:

Quintessence Wealth, a registered Portfolio Manager in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, Quebec, and Saskatchewan, an Investment Fund Manager in Newfoundland and Labrador, Ontario, and Quebec, and an Exempt Market Dealer in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Quebec, and Saskatchewan. The Ontario Securities Commission (OSC) is the principal regulator for Quintessence Wealth.

The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. The information contained herein may not apply to all types of investors. The opinions in this market outlook were prepared by Alfred Lee as of the date of this report and are subject to change without notice. The opinions expressed in this report are that of the author and do not necessarily reflect the opinion of Q Wealth as a firm. This report is not to be construed as an offer or solicitation to recommend Q Wealth products to clients.