Last Wednesday, both the Bank of Canada (BoC) and the U.S. Federal Reserve (Fed) delivered the rate cuts markets had been anticipating — each lowering their policy rate by 25 basis points.

While the outcome was expected, the underlying rationale, and the path forward from here, diverge sharply on each side of the border.

Canada: A Justified Course Correction

The BoC’s decision comes amid mounting evidence of a cooling Canadian economy. Real GDP growth has slowed to just 0.9% year-over-year, headline CPI has decelerated to 1.7%, and unemployment has risen to 6.9%.

Notably, Governor Tiff Macklem offered very little in the way of forward guidance or a clear rate path going forward, emphasizing only that the recent tariffs have had a negative impact on the Canadian economy. That restrained tone leaves markets without a strong signal on whether this marks the start of a cutting cycle or a one-off recalibration.

In short, Canada had room to ease — and reason to do so.

Canadian Economy Showing Clear Signs of Slowing

Source: Bloomberg, CPI data as of August 2025, GDP and Unemployment as of June 2025

United States: A More Delicate Situation

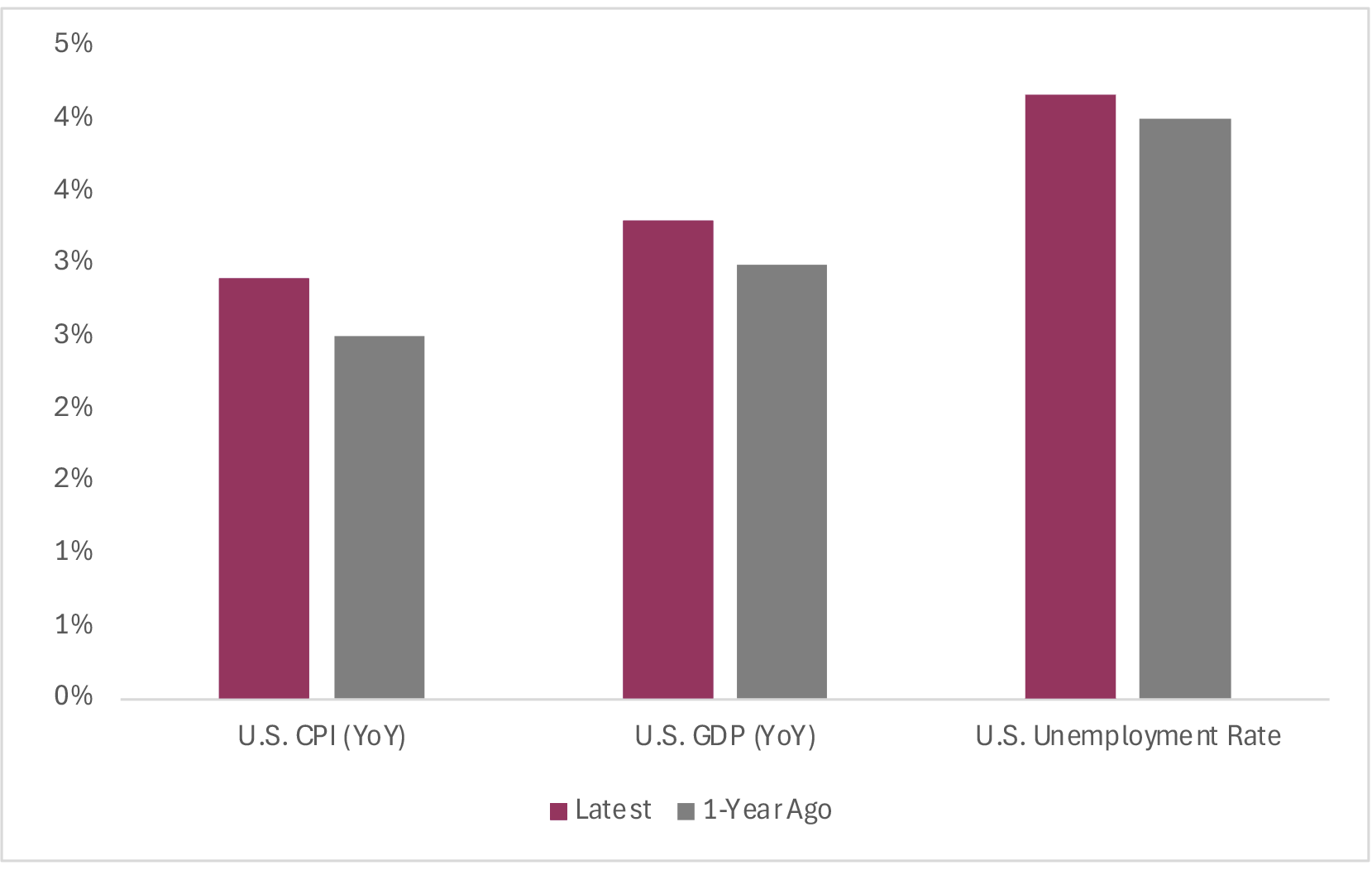

The Fed’s cut is far more contentious. The U.S. economy remains remarkably resilient, with GDP expanding at 3.3% quarter over quarter (annualized) and inflation still hovering at the top end of the Fed’s 2% target range.

While the Fed pointed to global uncertainty, tariffs, and a weakening jobs market, cutting rates while inflation remains elevated carries significant risk.

When the spectre of stagflation emerges, central banks must prioritize fighting inflation over propping up growth. Policymakers have far more tools to stimulate the economy if growth slows, but very few to contain inflation if it accelerates. Once inflation expectations become unanchored, the cost of regaining credibility can be steep.

U.S. Economy Slowing but Still Robust

Source: Bloomberg, CPI data as of August 2025, GDP and Unemployment as of June 2025

📚 Lessons from History

History shows just how dangerous it can be to cut rates in the face of rising inflation. The Fed has done so only a handful of times — 1974–75, spring 1980, and 2007–08. Each episode ended poorly: either inflation re-accelerated (1970s, 1980) or financial instability forced further cuts even as inflation continued to climb (2007–08).

The lesson is clear: cutting into rising inflation is unusual and typically ends with the Fed forced to reverse course. While we remain constructive on markets, a too-dovish Fed would risk overheating asset prices and destabilizing the foundations of the current bull market. It was critical that the Fed did not come in more dovish than markets were already expecting.

⚖️ The Politics and Perception Problem

Markets have also been mindful of growing political pressure on the Fed heading into the 2026 U.S. mid-term elections.

While some point to early signs of labour-market softening, it’s important to remember that taming inflation inevitably involves some economic pain. A central bank’s willingness to tolerate that pain is what gives it credibility.

If the Fed appears to be acting at the behest of the administration, it risks damaging the market’s perception of its independence. That perception anchors long-term rates. Lose it, and investors may demand higher yields on longer-dated bonds to compensate for future inflation risk — effectively tightening financial conditions even as the Fed tries to loosen them.

📈 Asset Prices Tell Their Own Story

While the Fed maintains that it does not target asset prices, the fact that stocks, gold, and even bitcoin are at or near record highs is telling. These market signals point to ample liquidity still coursing through the system — hardly the backdrop in which further easing is warranted.

Asset markets thrive when money is cheap. But if asset inflation becomes detached from fundamentals, it risks fueling instability down the road.

🔭 Looking Ahead: Guidance Was the Real Story

While Powell likely did not fully avoid the perception that the Fed is bending to political pressure, the neutral and measured tone of the announcement helped contain that narrative and preserve some policy credibility. He reiterated the importance of Fed independence, though it marked a notable shift from the more hawkish tone he struck just a few months ago.

Importantly, he did not push back against market expectations for two additional quarter-point cuts later this year. In our view, leaving those expectations unchallenged carries the risk of fueling inflationary pressures, especially with financial conditions already loose and asset prices near record highs.

Eyes will now have to remain firmly on inflation. While Wednesday’s cut was largely expected, continuing to ease policy into an environment of strong growth and still-elevated prices could risk reigniting inflation and undermining the Fed’s hard-won credibility.

✅ Bottom Line

While the BoC’s cut was well-justified, the Fed’s move was far more debatable. Both central banks will now need to carefully manage market expectations and reassert their commitment to price stability.

Because ultimately, credibility is their most powerful policy tool — and once lost, it is extraordinarily hard to get back.